Ray White Group Chief Economist, Nerida Conisbee, revealed that rate cuts have impacted coastal lifestyle markets, premium suburbs and now affordable outer areas at different times.

“Australia has experienced three major interest rate cutting cycles since 2015, each delivering vastly different impacts across the housing market,” Ms Conisbee said.

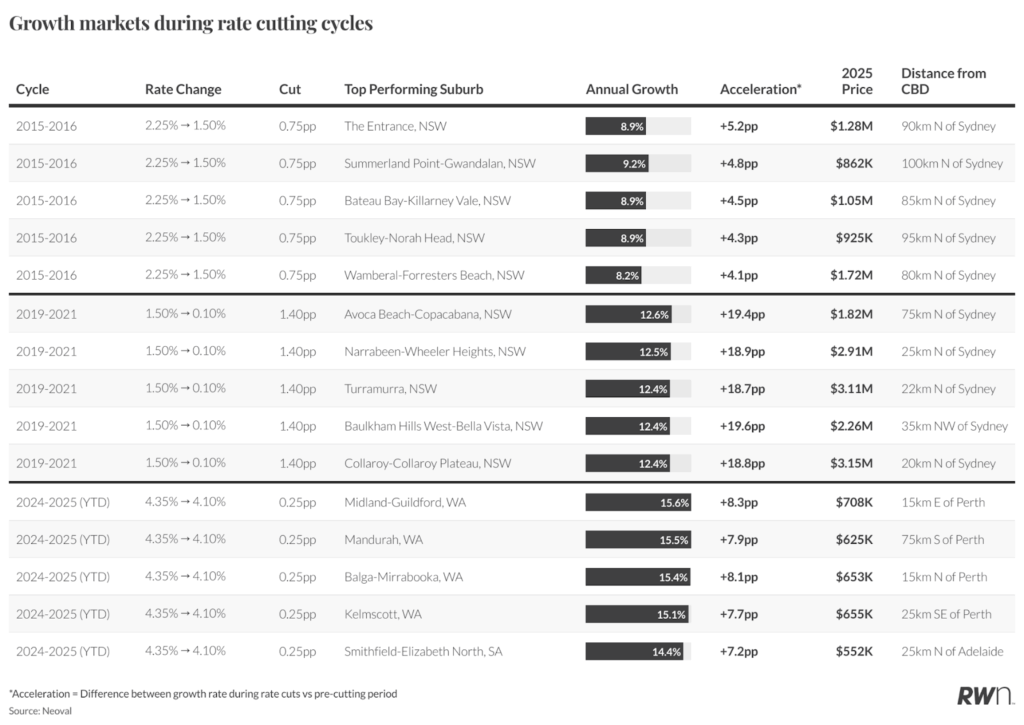

“The Reserve Bank’s gradual easing from May 2015 to May 2016 saw rates fall from 2.25 per cent to 1.50 per cent, followed by the aggressive cuts from June 2019 through the COVID emergency period that took rates from 1.50 per cent to a historic low of 0.10 per cent by late 2020.”

Ms Conisbee said that the current cutting cycle, beginning in 2024 from multi-year highs above 4 per cent, represents the third distinct easing phase in a decade.

The analysis measured rate cut sensitivity by comparing annual price growth during cutting periods against pre-cutting baseline growth, with “acceleration” calculated as the difference between these growth rates.

During the 2015-2016 cycle, coastal lifestyle markets within commuting distance of major cities emerged as the main winners.

“The first cutting cycle from May 2015 to May 2016 saw the Reserve Bank reduce rates by 0.75 percentage points in response to moderating economic growth and subdued inflation,” Ms Conisbee said.

“This gradual easing primarily benefited coastal lifestyle markets within commuting distance of major cities, with NSW’s Central Coast emerging as the standout performer.”

Areas such as Avoca Beach-Copacabana (8.0 per cent growth), Wamberal-Forresters Beach (8.2 per cent), and The Entrance (8.9 per cent) led the market response during this period.

The 2019-2021 cycle, which included the COVID emergency period, saw a shift in which areas benefited most from rate cuts.

“The most aggressive cutting cycle began in June 2019, then accelerated dramatically during the COVID emergency period as rates plunged from 1.50 per cent to 0.10 per cent,” Ms Conisbee said.

“These unprecedented rate cuts led to the strongest responses in Sydney’s premium suburbs, with areas like Turramurra (12.4 per cent growth in 2019-2020), Castle Hill precincts (over 12 per cent), and Northern Beaches locations including Collaroy-Collaroy Plateau and Freshwater-Brookvale all posting double-digit gains.”

The biggest acceleration occurred in Castle Hill areas, where suburbs like Baulkham Hills West-Bella Vista swung from -7.2 per cent growth to +12.4 per cent, representing a 19.6 percentage point acceleration.

In contrast, the current 2024-2025 cutting cycle has fundamentally reversed previous patterns, with affordable outer suburban areas now seeing the greatest benefit.

“The current cutting cycle, beginning from the highest rates in over a decade, has fundamentally reversed previous patterns by most benefiting affordable, outer suburban areas,” Ms Conisbee said.

“Perth has dominated this cycle, with areas like Midland-Guildford (15.6 per cent growth), Mandurah (15.5 per cent), and Balga-Mirrabooka (15.4 per cent) leading national growth rates.”

Adelaide’s outer suburbs have also responded strongly, with Smithfield-Elizabeth North posting 14.4 per cent growth.

These areas, typically priced between $550,000 and $750,000, represent traditional first home buyer territories.

Ms Conisbee said that the evolution of rate cut winners reveals fundamental changes in Australia’s housing market.

“From emerging coastal lifestyle markets in 2015-2016, to premium Sydney suburbs during the COVID emergency, to affordable outer areas today, each cycle is different,” she said.

“The Central Coast’s consistent performance across all cycles suggests certain markets maintain enduring rate sensitivity, but the dramatic swing from million-dollar suburbs to sub-$750,000 areas demonstrates how affordability constraints now dictate market responses.”