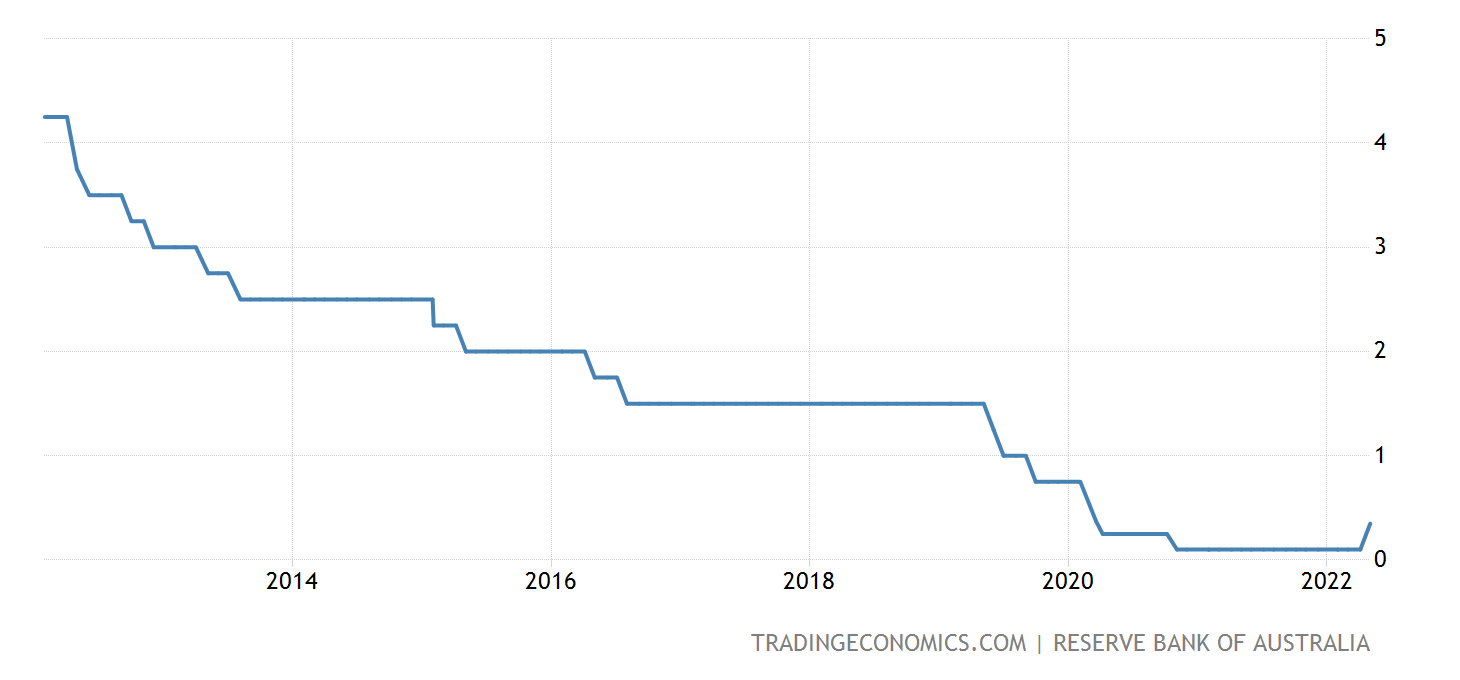

After 17 months of record low interest rates, the Reserve Bank of Australia has today lifted the cash rate 25 basis points to 0.35 per cent while clearly indicating more rate rises are to come.

Although widely expected, today’s upward move signals the bank’s intention to wind back the monetary support put in place to assist the Australian economy during the pandemic.

It also comes in response to high inflation, a record low unemployment rate, and household and business balance sheets that Reserve Bank Governor Dr Philip Lowe describes as being “in generally good shape”.

“The economy has proven to be resilient and inflation has picked up more quickly, and to a higher level, than was expected,” Dr Lowe said.

“There is also evidence that wages growth is picking up. Given this, and the very low level of interest rates, it is appropriate to start the process of normalising monetary conditions.”

Although lower than many other advanced economies, Australia’s inflation rate currently sits at 5.1 per cent, or 3.7 per cent in underlying terms.

“This rise in inflation largely reflects global factors,” Dr Lowe said.

“But domestic capacity constraints are increasingly playing a role and inflation pressures have broadened, with firms more prepared to pass through cost increases to consumer prices.

“A further rise in inflation is expected in the near term, but as supply-side disruptions are resolved, inflation is expected to decline back towards the target range of 2 to 3 per cent.”

Dr Lowe said the central forecast for 2022 was a headline inflation of around 6 per cent and underlying inflation of around 4.75 per cent.

“By mid 2024, headline and underlying inflation are forecast to have moderated to around 3 per cent,” he stated.

“These forecasts are based on an assumption of further increases in interest rates.”

Inflation might be higher than previously expected but Dr Lowe noted the resilience of the Australian economy was evident in the labour market.

Over recent months, the unemployment rate has declined to 4 per cent and is forecast to further decline to around 3.5 per cent by early 2023, and remain at that level.

“This would be the lowest rate of unemployment in almost 50 years,” Dr Lowe noted.

Although stating the outlook for economic growth in Australia remained positive, Dr Lowe said there were still ongoing global uncertainties.

These include: the ongoing disruptions from COVID-19, especially in China; the war in Ukraine; and declining consumer purchasing power from higher inflation.

“The central forecast is for Australian GDP to grow by 4.25 per cent over 2022 and 2 per cent over 2023,” Dr Lowe said.

“Household and business balance sheets are generally in good shape, an upswing in business investment is underway and there is a large pipeline of construction work to be completed.

“Macroeconomic policy settings remain supportive of growth and national income is being boosted by higher commodity prices.”

One of the key indicators the RBA was examining prior to raising the cash rate was wages growth.

Dr Lowe said it now appeared this was picking up.

“In a tight labour market, an increasing number of firms are paying higher wages to attract and retain staff, especially in an environment where the cost of living is rising,” he noted.

“Given both the progress towards full employment and the evidence on prices and wages, some withdrawal of the extraordinary monetary support provided through the pandemic is appropriate.

“Consistent with this, the Board does not plan to reinvest the proceeds of maturing government bonds and expects the Bank’s balance sheet to decline significantly over the next couple of years as the Term Funding Facility comes to an end.

“The board is not currently planning to sell the government bonds that the Bank purchased during the pandemic.”

Dr Lowe concluded the RBA board remained committed to doing what was necessary to ensure inflation in Australia returned to target over time.

“This will require a further lift in interest rates over the period ahead,” Dr Lowe said.

“The board will continue to closely monitor the incoming information and evolving balance of risks as it determines the timing and extent of future interest rate increases.”

Nigel O’Neil – Barry Plant Group

Barry Plant Group Chief Executive Officer Nigel O’Neil said today’s cash rate increase was a sign of things to come, with rates likely to rise further over the coming months.

Mr O’Neil said today’s increase of 0.25 per cent was moderate compared to what he had anticipated.

“Based on the recent inflation figures, my expectation was an increase of 0.4 per cent to take the cash rate to 0.5 per cent,” he noted.

“The likelihood is they will increase a further 0.25 per cent next month and we will see a base rate of 2 per cent by the end of next financial year.”

For home buyers and existing mortgage holders, Mr O’Neil said they should be factoring that rise into their decision-making.

For agents discussing the rate rise with nervous buyers, Mr O’Neil said it was important to keep things in perspective.

“Money is still cheap. There are current rates that still have a 2 in front of them, and within 12 to 18 months they are likely to start with a 4,” he said.

“That’s still affordable when you consider not that long ago, interest rates were in the double digits.”

Mr O’Neil also said he had expected the RBA to raise rates sooner, given the average Australian was feeling the hit of high inflation.

“Every man and his dog could tell the cost of living was accelerating,” he noted.

However, he continued it was good to see the RBA increase the cash rate this month in a sign they were independent of the political process and a pending election.

As for whether today’s cash rate rise would impact the election result, Mr O’Neil said he doubted it would.

“I think people have made up their mind already,” he said.

“And they were also expecting this increase.

“A 0.25 per cent is a modest increase, but it’s what coming that people should keep in mind and they should factor in further rises over the next 12 months.”

Geoff Lucas – The Agency

The Agency Managing Director and Chief Executive Officer Geoff Lucas said today’s rate rise was not a surprise, despite coming slightly earlier than many economists had predicted.

He said recent inflation figures of 5.1 per cent had also foreshadowed the RBA’s actions.

“I wasn’t surprised given the recent strong inflation figures and especially given that the RBA told us today that they didn’t need economic data, they’ve cited some acceleration in wages in the private sector via their business liaison services,” Mr Lucas said.

“They’ve been out proactively seeking information and cited some strong wage growth, all of which are healthy signs for the economy.”

In terms of the impact on the real estate market, Mr Lucas said the prospect of rate rises had already been baked into the market as evidenced by CoreLogic statistics released earlier this week showing national sales volumes were down 11.6 per cent for the first four months of the year.

“I think that’s an indicator that the upward movement in rates is already baked into sentiment,” he said.

“We continue to expect there will be additional new listings post the election, but that the time it takes to transact those listings will likely increase.

“Days on market have been starting to increase and we’d expect that will continue because the consumer sentiment will be, ‘I can buy at a lower rate later on’.”

Mr Lucas said while rates were still coming off historical lows, there had been 200 basis point movement of bank fixed rates in the past six months and that had to be taken into account.

However, he said today’s rate rise, along with the media coverage given to it, would have an impact.

“You’ll see another surge of negative sentiment as a result of that,” Mr Lucas said.

“It will be a case of reality striking now that it’s actually happened. The reality of seeing it in print in front of people will possibly create greater negative sentiment than has already been baked in.”

But Mr Lucas said there was one potential positive to come out of today’s cash rate climb and that was for aspirational homebuyers previously disheartened by continuing property price rises to gain renewed hope of entering the market.

“It will possibly reignite enthusiasm, or in fact the belief that entry into the housing market is possible,” he said.

“They’ve been disengaged and falls in prices, I know it’s off the back of extraordinary increases, may reignite the hope of aspirational homebuyers, which is a health thing for the market.”

Manos Findikakis – Eview Group

Eview Group Chief Executive Officer Manos Findikakis said he expected today’s long foreshadowed cash rate rise.

“There will be a little bit of a disruption in confidence, for a very short period of time,” he said.

“Having said that, from a financier’s point of view, and for those people that have borrowed in the past 12 months, I think it was already factored in.

“The hoops you had to jump through to obtain finance over the past 12 months, they’ve already factored it in, making sure people’s affordability was there for the imminent rate increases that we’re going to experience.”

Mr Findikakis said after the initial disruption in confidence and the Federal Election, he expected to see a strong spring property market with prices continuing to curtail around the current 0.1 per cent rate, but didn’t anticipate anything dramatic.

He said he also expected to see upward pressure on wages and people’s pay packets gradually climbing.

“Every business owner that I’m speaking to is increasing their budget for attracting talent, so that automatically increases the pressure on wages,” Mr Findkakis said.

“Employees are also talking to their fellow employees who are getting wage increases, and it has a snowball effect.”

Mr Findikakis said in the real estate arena there was a shortage of talent.

“There’s strong poaching and strong competition between businesses to attract the good talent,” he said.

He said his business was looking at making more formal the work from home conditions used during the pandemic as a means for attracting talent.

“Being an employer of choice is no longer just about pay,” Mr Findikakis said.

“It’s as much about working conditions as it is about pay.”

Mr Findikakis said while he didn’t have a crystal ball, he expected the RBA to continue lifting interest rates in the coming months.

“Everyone needs to factor in a 2 per cent to 3 per cent rate rise over the next 12 months,” he said.

Andrew Cocks – Richardson & Wrench

Richardson & Wrench managing director Andrew Cocks noted the RBA’s cash rate rise came as little surprise but conceded announcing the increase less than three weeks from an election was a move away from some long-established precedents.

“It’s been 15 years since official interest rates were increased during the election campaign of Kevin ‘07,” Mr Cocks reflected.

“And it’s been 139 months or almost half a generation since the last hike in interest rates.”

Mr Cocks said strong CPI results had forced the RBA’s hand, but the rise was low, considering the current climate

“The 0.35 per cent cash rate is well below the long-term average over the last few decades which is sitting just below 4 per cent.

“The interesting thing about the latest RBA move is that it doesn’t precede a turn-around in Australia’s property markets, which had already started to experience some softening in recent months and are likely to continue to move back to more normal settings over the years ahead.”

Mr Cocks said the shocks experienced by Australia’s real estate markets over the last couple of years had been significant and abnormal.

“The fact that they have performed as well as they have is a testament to the strength of the fundamentals that exist, and will continue to exist, in the Australian economy for the foreseeable future.

“There’s a high standard of living, high standard of education, high standard of safety and security, low unemployment, high wages by international standards, and world leading and diverse contributors to the GDP.

“All of these ingredients mean that Australia is incredibly well positioned to expand significantly over the next few years, even with the current supply chain and workforce shortages that are being experienced at the moment.

“These will pass as the Covid impacts wash through the global economy over the next few years.”

Looking to the future, Mr Cocks said the big uncertainty facing the property markets moving forward was how the unusual changes forced onto the economy over the last couple of years were unwound.

“There is a risk that hitting the brakes too hard could see Australia sling-shot from strong growth to a far more challenging environment,” he noted.

“Australian property owners are well-positioned to deal with a few interest rate increases.

“The pandemic induced ‘savings plan’ has seen many Australians build up a significant buffer of savings over the last few years, and the vast majority of loans have been written with a higher interest rate scenario built into the serviceability assessments.

“There is no question that the Australian property market was operating way above long-term averages and it is a good thing that we’ve started to see some winding back of the abnormal behaviours.

“But the risk that those controlling policy have to balance is the need to make sure that they don’t overshoot and push Australian borrowers beyond their capacity thereby creating another abnormal market on the other side of the curve.”

Real Estate Institute of Australia

The Real Estate Institute of Australia (REIA) has urged calm following the rate rise to 0.35 per cent, which is expected to have a moderate impact on housing affordability Australia-wide.

REIA President Hayden Groves said the increase in the cash rate would have a modest impact on affordability, with banks and mortgage holders well prepared.

“Wages are expected to increase offsetting a rise in home loan payments where they are passed on by banks and market indications are that house prices will continue to stabilise,” he said.

“Aspiring home buyers will not be facing the extreme growth experienced since the onset of the COVID-19 pandemic so there is no need for those hunting for a home to put those plans on hold.”

Mr Groves added that the increase is the first since November 2010 and that banks and mortgage holders are well prepared for an even higher interest rate environment.

“If the cash rate rises to the 2.1 per cent forecast, the proportion of median income required will rise by 6.2 per cent, which most financial institutions would have already stress tested applicants for such rises,” he said.

“That being said, with market economists forecasting a cash rate of at least 2 per cent by mid next year, if wages don’t increase it could be a completely different scenario which will see affordability at its worst in more than a decade,” he cautioned.

Mr Groves said the rise in interest rates reiterated the urgent need for a national plan that addresses housing affordability and supply which should be supported by both federal and state governments.

“While we support current government policies being presented during the election campaign and previous plans from the current government, prohibitive taxes such as the extremely high stamp duty payments are a key concern in limiting supply and affordability,” he said.

Mathew Tiller – LJ Hooker

LJ Hooker said the RBA’s decision to increase interest rates for the first time in more than a decade would have little impact on the property market.

LJ Hooker Group Head of Research Mathew Tiller said the RBA was confident the economy, buoyed by strong employment figures and rising wages, could withstand the rate increase to 0.35 basis points.

On a mortgage of $1 million this equates to around an extra $208 per month. And on a mortgage of $500,000 this equates to around an extra $108 per month.

“Any effect on the property market will be minimal given only 35 per cent of households in Australia own a property with a mortgage and that we have seen such strong value growth right across the country,” Mr Tiller said.

“We are not expecting to see a flood of listings as a result of today’s announcement by the RBA. We have seen strong price growth since the pandemic and for those who acquired a property more than 12 months ago, they have seen an increase in the equity and capital in their homes.”

Mr Tiller said first home buyers who stretched themselves to purchase in the past few months may feel a little nervous, however, employment security ensures that people should still be able to afford to pay their mortgage.

Speculation in the media about rate increases has also mentally prepared mortgage-holders for the inevitable, he noted.

During the pandemic household savings have increased, while many have taken advantage of the historic low levels to pay down their mortgage.

“We are not having an increase in mortgage rates at a time when people are losing their jobs and can’t afford to make their repayments – the economy is doing well,” Mr Tiller said.

“The RBA believes it can handle an interest rate rise and will effectively dampen rising inflation which this week hit the highest levels seen in 20 years. Now it is a waiting game to see how the banks will determine how much of a rate rise they will pass onto their customer.”

Raine & Horne

Experts from Raine & Horne said homeowners shouldn’t expect the sky to fall in as a result of today’s cash rate increase.

“The Australian Central Bank last increased the official cash rate on 3 November 2010,” Raine & Horne Executive Chairman Angus Raine said.

“To put this into a historical perspective, Julia Gillard was the Australian Prime Minister at the time of the last rate rise.

“However, whether it is a 0.25 per cent or a 0.40 per cent increase, the lenders currently apply a buffer of 3 percentage points to your interest rate when calculating a borrower’s ability to service a home loan.”

Senior Finance Specialist at Raine & Horne’s financial services division Craig Betalli said most banks assessed borrowers’ capacity at around 6 per cent interest rates.

“We are expecting that the banks will increase these buffers,” he said.

Mr Betalli said borrowers were still clearly better placed than when the RBA tightened monetary policy, with the cash rate increasing to 4.75 per cent, almost 12 years ago.

“With rates falling to a historical low of 0.10 per cent due to the pandemic, people who were unaffected by COVID lockdowns used the lower rates and additional borrowing capacity to upgrade or improve their homes. Also, first home buyers and investors have all been active in the market.”

According to Mr Betalli, with more Australians now carrying more borrowings, the RBA will hesitate to make significant changes to monetary policy.

“It will be difficult for the RBA to ramp up interest rates significantly to control inflation, as substantial increases will hurt borrowers and the economy,” he said.

“Therefore, any talk of significant interest rate increases would seem wide of the mark.

“It’s fair to expect two to three interest rate increases before Christmas, at which point the RBA may take a wait and watch approach.”

Paul Ryan – PropTrack

PropTrack Economist Paul Ryan said today’s cash rate rise signalled the RBA was prepared to act to curb rising inflation and sought to remain independent of politics in the lead-up to the Federal Election.

“Inflation has proven to be both stronger as well as broader than the RBA expected, indicative of stronger domestic demand,” he said.

“There have also been increases in measures of inflation expectations, and significant reporting of inflationary pressures.

“The RBA’s internal indicators of wages growth have also picked up, so they expect official indicators of wage growth to follow shortly.

“By moving today, rather than waiting for further data in June, the RBA is signalling that it will intervene to curb stronger than expected inflationary pressures, despite the ongoing federal election campaign. While the RBA seeks to remain independent from politics, failing to adjust policy may have been viewed as a greater political intervention.”

Mr Ryan said while today’s increase was small it signaled the start of a series of rises before the end of the year.

“This will weigh on housing price growth, which has clearly slowed in anticipation of these higher borrowing costs,” he said.

“The outlook for housing prices later in the year is one of a balance between higher mortgage rates and the higher income growth the RBA is looking to see before raising rates.

“Later this week the RBA will update their forecasts for economic growth and inflation in light of this policy change and recent inflationary pressures.”

Sarah Megginson – Finder

Senior Editor of Money at Finder, Sarah Megginson, said one in five economists had correctly predicted today’s cash rate move in its Finder RBA Cash Rate Survey.

She said the rate rise is likely to lead to further hikes in home loans.

“This rate rise, along with a property market that is beginning to cool, means some recent buyers may be caught out now – or when their fixed rate ends,” Ms Megginson said.

“If your rate has jumped or looks like it is going to, it might be time to go home loan shopping and find a better interest rate.”