Pete Wargent, COO of property buyer’s agent platform BuyersBuyers.com.au, says that the housing market landscape has shifted quickly over the past three months, with prices now rising across the capital cities and buyer sentiment surging.

Mr Wargent said inquiry has picked up strongly over the past six weeks, initially from first homebuyers, but now also from investors.

“We expect to see a strong 2021 for housing, with more and more investors coming back into the market.

“With investment loans now available in the 2 to 3 per cent range, comparatively speaking yields are now looking more attractive in many areas, and the investors are returning,” Mr Wargent said.

“Some markets, such as houses in Brisbane, are noticeably picking up,” he added.

Doron Peleg, CEO of RiskWise Property Research said the group’s latest quarterly forecasts reflected the improved market conditions, stimulatory settings, and the successful containment of COVID-19 in Australia.

“While some risk areas of the market remain, especially in some of the oversupplied unit segments of the market, overall, 2021 is set to be a strong year of capital growth in Australian property,” Mr Peleg said.

Q4 2020 Risks & Opportunities Report: Summary or RiskWise findings

The landscape of the housing market has shifted rapidly in the past three months from a buyer’s market to a seller’s one.

Consequently, strong house price growth is forecast for 2021.

| City | 2021 forecast |

| Sydney | 8-12pc |

| Melbourne | 8-12pc |

| Brisbane and SEQ | 6-10pc |

| Perth | 4-8pc |

| Adelaide | 5-8pc |

| Canberra and ACT | 5-8pc |

With regards to COVID-19, several vaccinations are likely to be rolled out in 2021, providing confidence that a sustainable solution will ultimately be found.

A range of government measures have led to significant shifts in buyer confidence and house price expectations, particularly through September and October 2020.

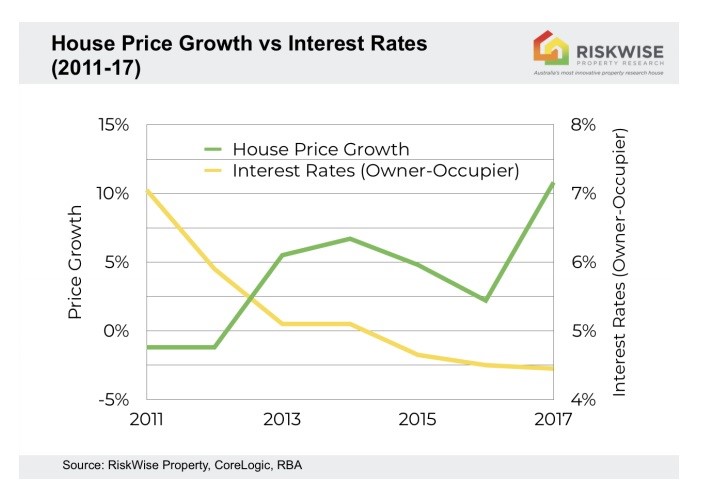

Alongside ultra-low interest rates, that make it typically cheaper to buy than to rent from a cashflow perspective, and proposed changes to responsible lending obligations, these measures have resulted in a materially increased demand for detached houses.

The traditional connection between lower interest rates and higher dwelling prices will be again seen in 2021.

With only a low availability of stock of quality assets in popular areas and increasing demand, this has been reflected by increasingly robust auction clearance rates, and it is projected that both Sydney and Melbourne will deliver capital growth in the range of 8-12 per cent in 2021.

Therefore, new highs for housing prices in Sydney and Melbourne are again on the horizon.

Houses versus units

Houses with a high land value component and scarcity value are likely to enjoy strong demand and capital growth, both in the short and long-term.

RiskWise market research shows that some sectors of the housing market continue to represent a high risk at the present time, in particular inner-city apartment markets, which are oversupplied and are experiencing falling rents as Australians look to avoid the higher density locations.

These risks, combined with high vacancy rates, increase serviceability (i.e. cash flow) risk, and consequently, make these apartments less attractive to investors, who represent the main cohort of buyers in those areas.

Population growth and external migration

As projected, our assumption that there will be significant reduction in total population growth due to low external migration, is still valid. The Federal government is expecting Net Overseas Migration (NOM) in FY21 to drop to -71,600 people, the first negative NOM since 1946.

This negative trend is forecast to continue in FY22 and only gradually return to pre-COVID levels from FY23 onwards.

The reduction in overseas migration has and will continue to have a major impact on rental apartments that have already experienced increased vacancy rates and lower demand from investors.

A stable jobs market is fundamental in external migration decisions. Consequently, poor economic growth and a soft employment market will see the attractiveness of relocation to Australia fall significantly, while border restrictions make movement logistically challenging

Sentiment improving sharply

The landscape of the property market completely changed from the beginning of September 2020, as mentioned above. Now, new peaks for Sydney and Melbourne are on the horizon and housing affordability is likely to deteriorate again.

Consumer sentiment, auction clearance rates and house price expectations

According to Westpac-Melbourne Institute, housing market sentiment surged in September and October, along with a sharp increase in Westpac’s House Price Expectations index, which lifted in September and October by 21.7 and 31.5 per cent, respectively.

The Westpac Consumer House Price Expectations Index tumbled 51 per cent in April in the first stages of the national lockdown. Yet more recently in October, Westpac’s key measure of house price expectations has risen strongly, by 31.5 per cent to 117.3 from 89.2 per cent.

All states have registered impressive recoveries. This followed a surge of 21.7 per cent in September.

While this index was still 6.5 per cent below the average level in the six months prior to COVID-19, it is highly likely that the index will rise materially in the next six months.

House price expectations are already being reflected in auction clearance rates figures.

Clearance rates across the country are likely to remain high and similar to pre-pandemic levels. With improved consumer confidence and auction clearance rates, it is likely that while volumes will materially increase in 2021, auction clearance rates will remain high, above the 70 per cent mark.

It should also be noted that the recovery through the COVID-19 pandemic is another demonstration that property is a long-term game and that houses and family-suitable properties in the larger capital cities tend to recover well after each major downturn.

State by state summary

NSW

A materially increased demand is expected for detached houses, with strong capital growth of 8-12 per cent forecast for Sydney.

Areas attracting lifestyle buyers include Byron Bay, the Central Coast (North Avoca, Terrigal, and Wamberal), the Hunter Valley, Wollongong, and the NSW South Coast. Beachside suburbs especially are outperforming the wider market.

Houses and units, particularly rental apartments, have a completely different risk profile.

The inherent risks of these two dwelling types that represent different buyer cohorts, are now being realised, with rental apartments carrying materially higher risk than houses, especially in some of the oversupplied locations of Sydney and the Central Coast detailed in previous RiskWise reports.

VIC

The most important developments since our August report have been Victoria’s outstanding success in almost eliminating COVID-19 and consequently the significant unwinding of restrictions across Victoria and the reopening of the VIC/NSW border.

As projected, the second wave of COVID-19 has had a major immediate impact. However, following the end of the pandemic, the Melbourne market has similar projections to Sydney, with a chronic undersupply driving land values higher, yet unit oversupply increasing both equity and serviceability risk.

The landscape of the housing market in Victoria has shifted rapidly, particularly in the past month, from a buyer’s market to a seller’s one.

Only three months ago home buyers in Melbourne were in solid position to leverage on the market conditions then, with very low volumes and low auction clearance rates.

This is, however, no longer the case, with a sharp increase in buyer sentiment and auction clearance rates.

Melbourne, once again, is presenting a similar trend to Sydney, with price growth projections in the range of 8-12 per cent in 2021.

However, investors who buy rental apartments in high supply areas are still taking a high risk with both equity and cashflow risk materially increasing, particularly in inner Melbourne.

QLD

The Sunshine State is shining – strong demand for detached houses and outstanding demand for lifestyle areas projected to deliver 6-10 per cent capital growth in 2021 for the southeast Queensland market.

The Queensland housing market, and particularly houses in the popular areas of Brisbane, the Sunshine Coast, and the Gold Coast, held up well during COVID-19, with the coastal areas enjoying strong demand due to the increased ability to work from home.

The Queensland Government has contained the virus very effectively. This, along with the increased ability to work remotely and ultra-low interest rates, boosted demand for houses in the Sunshine State.

During recent months, houses in the broader southeast Queensland area enjoy materially improved demand with improved consumer sentiment.

However, rental properties in high supply areas remain high risk. In Queensland houses are substantially preferred properties over units. Investors who buy rental apartments in high supply areas are still taking a high risk with both equity and cashflow risk materially increasing.

WA

Houses in Perth have finally bottomed out, and 4-8 per cent capital growth is forecast for 2021.

The most affordable capital city houses in the country are enjoying ultra-low interest rates, improved economic conditions and strong government incentives on the way to the recovery of the property market.

The Western Australian housing market experienced, prior to COVID-19, some improvement in buyer confidence along with signs of improvements in housing finance, is now enjoying strong government support that is a key driver in the improved economic conditions and renewed demand for housing.

Since the peak of the mining boom, the WA economy has experienced low economic growth, high employment that was well-above the 10-year benchmark, and consequently, very low population growth that resulted in low demand for residential properties.

This has led to continued price reductions, that made Perth the most affordable housing market in Australia with a median house price of $456,000.

The WA state government has provided a $444 million housing stimulus package to support the local economy. This package includes $319 million for social housing, which will refurbish 1500 homes, build and purchase approximately 250 new dwellings, and deliver a regional maintenance program to 3800 homes.

Other parts of the housing stimulus package include a $20,000 (additional) grant for first home buyers for new residential homes as well as a 75 per cent rebate for stamp duty that could take the available Federal and State grants for first home buyers close to $70,000.

The combination of the improved economy, government incentives, the recent reductions in interest rates, (with some lenders offering home loans with an interest rate below the 1.90 per cent mark), make WA substantially more attractive market, particularly for owner-occupiers.

For owner-occupiers with interest-only loans, ultra-low interest rates make it typically cheaper to buy than to rent a house from a cashflow perspective in all areas of Perth.

Units, however, particularly rental apartments in high supply areas, carry a higher level of risk.

ACT

The most resilient property market in the country will continue to enjoy solid price growth.

Units, however, are underperforming the wider market. The ACT has been enjoying extremely strong employment figures which are a key driver in the ability of the property market to deal very well with negative shocks, such as the recent downturn, and to deliver solid price growth under ‘normal’ market conditions.

Strong economic growth and an extremely robust employment market in the ACT with an unemployment rate of 3.7 per cent, ensured houses were strong performers, although the glut of new units presented a higher risk.

The ACT market showed a healthy price growth of 9.3 per cent for houses and 5.5 per cent for units in the past 12 months and had, prior to COVID-19, a good medium to long-term outlook.

Even the unprecedented COVID-19 has had only little impact on the ACT market with only a decelerating price growth. The government is a major direct and indirect employer in the ACT.

SA

Ultra-low interest rates, very affordable housing and strong response to COVID-19 are projected to deliver 5-8 per cent price growth in 2021.

The SA housing market that has been soft overall with modest growth (except for some areas), is showing clear signs of improved buyer confidence, demand for housing and consequently price growth projections.

Prior to COVID-19 the labour market was relatively soft with a reduction in actual employment which meant slow growth for dwelling prices until 2019.

At the beginning of 2020, however, buyer confidence increased, particularly in Adelaide, and this saw an improvement in auction clearance rates and, consequently, it appeared dwelling prices had reached the bottom.

As expected, COVID-19 has materially increased the unemployment rate, which negatively impacts the residential property market.

Also, the recent bushfires have also had a material impact on the demand for residential properties in South Australia’s affected areas.

However, in recent months, the market is leveraging on the improved demand prior to COVID-19, combined with ultra-low interest rates that make it cheaper to buy then rent.

For owner-occupiers with interest-only loans, ultra-low interest rates make it typically cheaper to buy than to rent from a cashflow perspective in all of Adelaide.

TAS

Lifestyle and limited supply of houses will continue to drive price growth in Hobart.

As previously projected, price growth in Tasmania has decelerated.

Affordability issues, with preferred alternatives in Melbourne, created a situation where the Apple Isle became less resilient and the property market continued to experience decelerated price growth despite low supply of dwellings.

While lifestyle changes have improved the demand for housing in Hobart, the market is likely to experience only modest price increases from this point.

Hobart is less attractive now to investors particularly in comparison to the Melbourne property market, which has demonstrated its strong economy fundamentals and appreciation of houses in the past 10 years.