Highlights

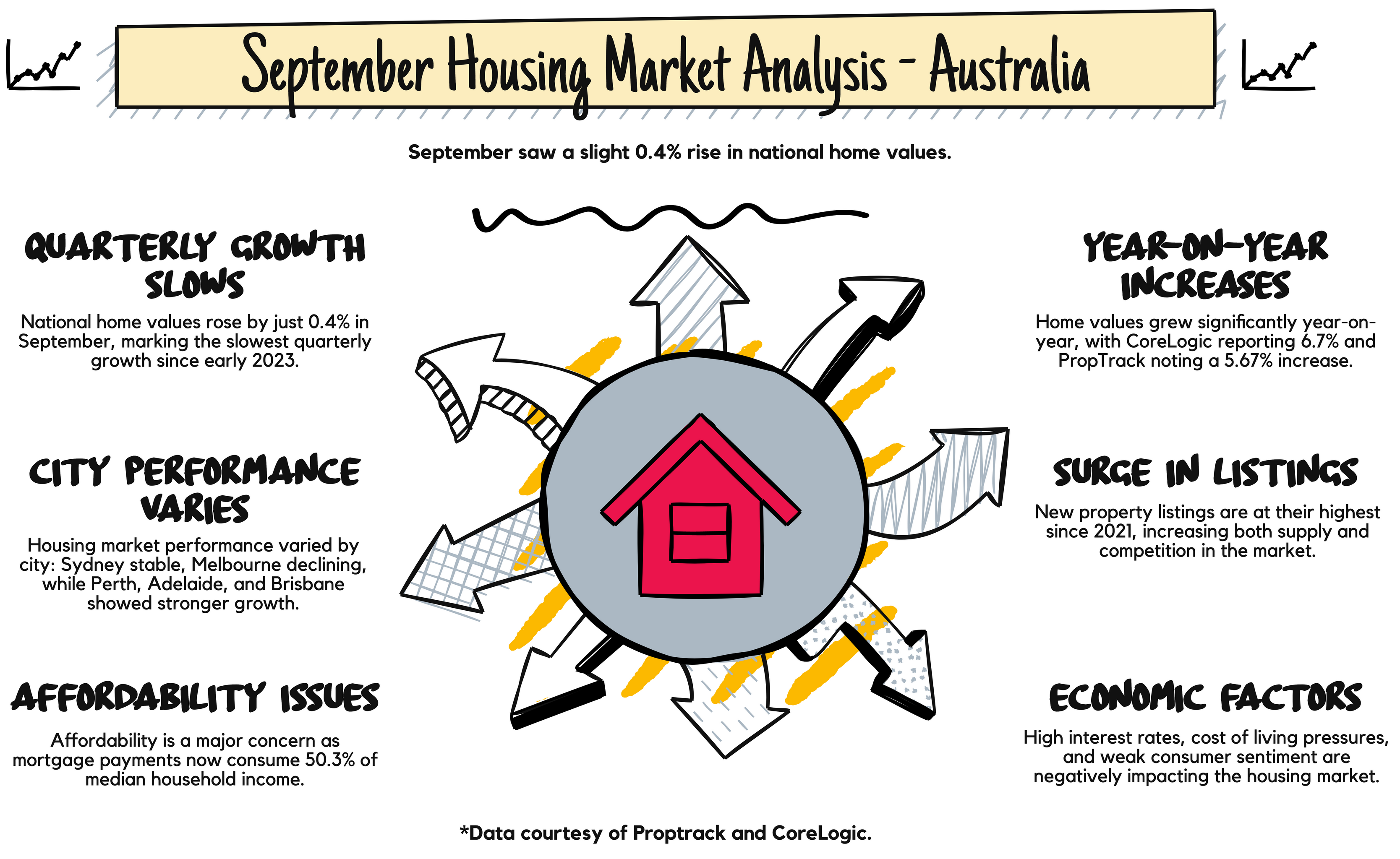

- National home values rose 0.4% in September, marking the slowest quarterly growth since early 2023.

- Year-on-year growth remains strong at 6.7% (CoreLogic) or 5.67% (PropTrack).

- Capital city performance varies: Sydney steady, Melbourne declining, Perth/Adelaide/Brisbane outperforming.

- New property listings have surged to levels not seen since 2021, increasing buyer choice and seller competition.

- Affordability remains a major challenge, with mortgage payments consuming a record 50.3% of median household income.

- Economic factors like high interest rates, cost of living pressures, and weak consumer sentiment are weighing on the market.

- Experts predict continued but slower growth, with potential interest rate cuts in late 2023 or early 2024 possibly boosting the market.

- Agents should consider local market conditions, realistic pricing for sellers, and decisive action for buyers when opportunities arise.

Listen to the Google Notebook LM “Deep Dive” Analysis of the September Numbers

The Australian property market continues to show signs of growth as we move through the Spring selling season, although slower than earlier in the year.

Recent data and expert insights from CoreLogic and PropTrack paint a picture of a cooling but still robust market with significant regional variations and ongoing affordability challenges.

National overview

According to CoreLogic, national home values rose by 0.4% in September, consistent with the growth rates observed in July and August.

PropTrack’s analysis aligns with this trend, noting, “The upswing in Australia’s home prices has persisted into the Spring selling season, though growth has slowed with buyers enjoying more choice.”

Despite this slowdown, the year-on-year growth remains substantial.

CoreLogic reports a 6.7% increase in national home values compared to last year, while PropTrack cites a 5.67% rise.*

Capital city performance

The momentum in capital cities is showing signs of fading, with some markets experiencing price declines.

CoreLogic data indicates that while Sydney remained steady, Melbourne led the decline with a 1.1% drop in dwelling values over the September quarter.

PropTrack, however, reported a more modest 0.3% decline in Melbourne for September.

Perth, Adelaide, and Brisbane continue outperforming other capitals, although growth in these cities is also easing. CoreLogic reported quarterly increases of 4.7%, 4%, and 2.7%, respectively.

Market drivers and challenges

As the spring selling season unfolds, a complex interplay of factors is shaping the Australian property landscape, presenting both opportunities and hurdles for buyers and sellers alike.

Tim Lawless, CoreLogic’s research director, highlighted the importance of the recent surge in property listings, noting that while it’s common in spring, this year’s levels have hit heights not seen since 2021.

“The rise in real estate inventory is a seasonal trend, with spring and early summer one of the busiest periods of the year for selling,” Mr Lawless said.

“However, the flow of freshly advertised housing stock hasn’t been this high at this time of the year since 2021.”

This influx of properties is creating a more balanced market, potentially shifting power dynamics between buyers and sellers.

“If the first month of spring is anything to go by, purchasing activity isn’t keeping pace with the flow of new listings,” said Mr Lawless.

“Markets where stock levels have lifted the most are unsurprisingly the weakest from a values perspective.

“A further rise in advertised supply is good news for buyers, but for vendors, it means more competition and the potential for a softening in selling conditions.”

While increased choice is a boon for buyers, affordability remains a significant hurdle.

CoreLogic reports that the portion of household income required to service a new mortgage for the median income household hit a record high of 50.3% in the June quarter.

This stark figure underscores the ongoing affordability crisis, with CoreLogic stating that “Housing remains unaffordable across every metric.”

The broader economic context is also playing a crucial role in market dynamics.

Eleanor Creagh, PropTrack’s Senior Economist, paints a picture of the multiple pressures at play.

“Though prices are rising, sustained high interest rates, cost of living pressures, weak consumer sentiment and affordability constraints are weighing,” Ms Creagh observes.

She adds that while buyers have more options, “uncertainty around the timing of interest rate cuts is likely also impacting the pace of growth.”

Interestingly, recent policy changes have injected some positivity into the market.

“July’s tax cuts boosted borrowing capacities and buyers’ budgets,” Ms Creagh said, suggesting that these measures, combined with persistent price growth, are “likely motivating some to overcome affordability challenges and transact.”

As the market navigates these competing forces, real estate professionals find themselves in a pivotal position, tasked with guiding clients through a landscape that’s both opportunity-rich and challenge-laden.

Outlook

Experts from both companies predict continued growth in housing values but at a slower and more geographically diverse pace.

Mr Lawless suggests a cut to interest rates is looking likely either early next year or even late this year. “This will provide a boost to borrowing capacity and should help to support a further lift in confidence to make high-commitment decisions like buying a home.”

Eleanor Creagh noted: “Ahead, prices are expected to lift through the typically busier spring selling season, albeit at a slower pace.”

FAQ: Spring property market update for real estate agents

As a real estate agent navigating the current market conditions, you may encounter various questions from clients. Here’s a quick reference guide to help you address common inquiries:

1. How is the property market performing this spring?

- National home values rose by 0.4% in September, according to CoreLogic.

- This growth rate is consistent with July and August, indicating a slowing trend.

- Year-on-year growth remains substantial at 6.7% (CoreLogic) or 5.67% (PropTrack).

- The market is still growing, but at a slower pace compared to earlier in the year.

2. Are there differences in performance across capital cities?

Yes, there are significant variations:-

- Sydney remains steady.

- Melbourne has seen a decline (1.1% drop over the September quarter, according to CoreLogic).

- Perth, Adelaide, and Brisbane are outperforming other capitals, with quarterly increases of 4.7%, 4%, and 2.7% respectively (CoreLogic data).

3. What’s happening with property listings?

- New listings have been surging, reaching levels not seen since 2021.

- This is partly due to the typical spring selling season trend.

- The increased supply is providing more options for buyers.

- It may lead to more competition among sellers and potentially softer selling conditions.

4. How is affordability affecting the market?

- Affordability remains a significant challenge.

- CoreLogic reports that the portion of household income required to service a new mortgage for the median-income household was at a record high of 50.3% in the June quarter.

- This affordability issue is impacting buyer behaviour and market dynamics.

5. What economic factors are influencing the market?

- High interest rates are affecting borrowing capacity.

- Cost of living pressures are impacting buyers’ ability to save and spend.

- Weak consumer sentiment is influencing decision-making.

- Recent tax cuts (July) have boosted some buyers’ budgets.

6. What’s the outlook for the rest of the year and early 2024?

- Experts predict continued growth in housing values but at a slower pace.

- The market is expected to become more geographically diverse in its performance.

- There’s potential for interest rate cuts either late this year or early next year, which could boost borrowing capacity and confidence.

- Further price lifts are expected during the spring selling season, albeit at a slower pace than in previous years.

7. What should I highlight to clients about this changing market?

- For sellers: Highlight the importance of realistic pricing given the increased competition.

- For buyers: Emphasise the greater choice available but the need to act decisively if they find a suitable property.

- For both: Stress the importance of understanding local market conditions, as performance varies significantly between regions.

- Keep clients informed about potential interest rate changes and their impact on the market.

* Why do CoreLogic’s and Proptrack’s numbers vary?

- The difference between CoreLogic and PropTrack’s annual growth (6.7% vs. 5.67%) and other figures is likely due to variations in data collection methods and calculations, property types included, timing, or geographical coverage.

Remember, market conditions can vary significantly at the local level. Always combine this general market information with your specific local market knowledge when advising clients.