The rental market is showing clear signs of transition, with new Domain data revealing that record-low vacancy rates are no longer translating into broad-based rent growth as affordability constraints begin to bind.

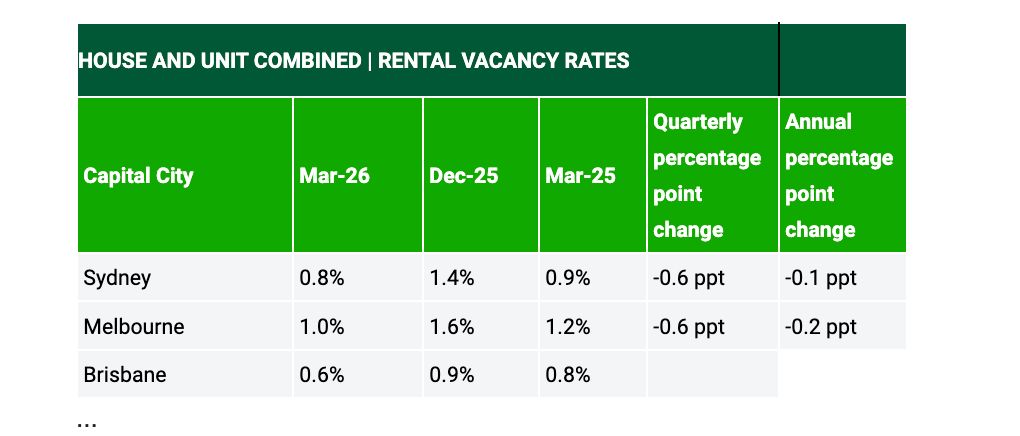

The Domain Rental Report (March 2026) shows national vacancy rates have fallen to a record low of 0.7%, underscoring continued supply pressure across capital cities. Despite these conditions, rent growth is no longer uniform, with several markets now showing signs of stalling.

Rental performance is increasingly fragmented. Perth is recording the strongest rebound in rents, Brisbane continues steady growth, while Sydney has flattened at record highs and Melbourne’s recovery remains uneven. Adelaide is also showing more seasonal than sustained growth patterns.

In Sydney, house rents remain at $800 per week, with unit rents at $750, marking the first sustained period in five years where rents have stalled despite extremely tight conditions.

According to Domain’s Chief Residential Economist Dr Nicola Powell, the market has now reached a clear affordability threshold.

“Three months ago, we warned that renters were running out of capacity to absorb higher rents. Even during the usually stronger March quarter, this month’s data shows that affordability ceiling has now been reached,” said Domain’s Chief Residential Economist, Dr Nicola Powell.

“Vacancy rates are lower than ever and supply remains incredibly tight, but rent growth is no longer accelerating everywhere. That tells us households simply can’t stretch any further.”

“In many cities, we’re seeing rents hold flat or rise unevenly despite worsening shortages. Affordability, not demand, is now the key constraint.”

Affordability now shaping rental outcomes

While supply remains extremely tight, renter behaviour is increasingly influencing outcomes, with households adjusting expectations, delaying decisions, and shifting location or housing type in response to cost pressures.

“What we’re seeing now is a clear disconnect between theory and reality. In theory, tight vacancy rates should allow landlords to keep pushing rents higher. In reality, many renters are simply at their financial limit.”

“Hitting an affordability ceiling doesn’t mean rents suddenly fall, but it does mean pricing power is weakening. The market is starting to self-regulate as renters push back, through longer decision times, negotiating harder, downsizing, sharing, or walking away altogether.”

Implications for landlords and agents

For landlords and agents, the data points to a market where aggressive rent increases are becoming harder to sustain without impacting vacancy and turnover outcomes.

“For landlords and agents expecting aggressive rent rises in 2026, the risk is overestimating demand elasticity. Pushing rents beyond what the market can bear can actually increase vacancy periods, tenant churn and leasing costs,” said Dr Powell.

“The more sustainable strategy from here is defensive rather than aggressive growth: prioritising long-term tenancy, minimising turnover, and recognising that even in undersupplied markets, affordability ultimately sets the ceiling.”

Agents urged to adjust leasing strategies

As renters become more price-sensitive and slower to commit, leasing strategies are shifting toward greater responsiveness and more realistic pricing from the outset.

“The biggest shift agents need to make is from a “list-and-lean-back” mindset to a far more responsive, renter-centric approach.”

“First, pricing needs to be realistic from day one. Renters are now highly informed – they’re comparing listings in real time, tracking days on market, and are far less forgiving of properties that feel overpriced.

“Second, speed and service matter more than ever. Slower commitment from renters means agents need to follow up faster, be clear on inclusions, respond immediately to enquiries, and reduce friction in the application process. The days of assuming a tenant will wait are over.”

Finally, Dr Powell said marketing needs to focus less on scarcity and more on value – things like energy efficiency, flexibility on lease terms, or small incentives that improve livability.

“In this phase of the cycle, renters are asking “Is this worth it?” not “Will I miss out?””

Affordability reshaping demand and creating new opportunities

While affordability is capping rent growth across much of the country, it is also reshaping demand in ways that are creating clearer opportunities across parts of the market, particularly in the unit sector.

Tighter household budgets are shifting renter priorities toward value, location and practicality, with more weight placed on affordability and liveability rather than competition for scarce stock.

“Affordability pressure is reshaping renter behaviour, and that’s creating very clear opportunities, particularly in the unit market.”

That shift is strengthening demand for well-located apartments close to transport, employment hubs and essential services, as renters trade down from higher-cost housing options.

For investors, that is translating into renewed interest in units with strong fundamentals.

“For investors, well-located apartments with strong fundamentals like access to transport, employment hubs and amenities are becoming increasingly attractive.”

At the development level, the changing environment is influencing design priorities, with a stronger focus on functionality and efficient living spaces.

“Developers have an opportunity to rethink products. Smaller, well-designed apartments that prioritise efficiency, storage and liveability rather than luxury finishes are far more aligned with today’s renter demand.”

For agencies, the shift is increasingly about managing higher leasing volume rather than chasing price growth, particularly in the unit sector where turnover is expected to remain elevated.

“There’s growth in volume rather than price escalation. Managing higher turnover in the unit sector, servicing build-to-rent style offerings, and positioning themselves as advisors on affordability-led demand will be critical.”

Looking ahead, Dr Powell said the most successful market participants will be those who adapt to affordability as a structural force rather than a short-term cycle.