Australia’s inflation has climbed to 4.6% over the year to March, reigniting pressure on the Reserve Bank as price growth broadens across housing, transport and food rather than easing in isolated pockets.

With fuel shocks amplifying short-term volatility and housing remaining the dominant structural driver, economists say the RBA is confronting a difficult trade-off: higher rates are slowing demand, but doing little to resolve the underlying supply constraints keeping inflation elevated.

Read what our experts had to say about RBA’s latest rate rise.

Nerida Conisbee, Ray White Group Chief Economist.

Ray White Group Chief Economist Nerida Conisbee has warned that the Reserve Bank of Australia’s latest interest rate hike presents a “difficult policy trade-off,” as the nation grapples with a housing-led inflation problem that rate rises alone cannot fix.

While the RBA has acted to anchor inflation expectations, she said that the move comes at a time when consumer confidence is already “extremely weak” and the labor market is beginning to show cracks beneath the surface.

The recent spike in pricing pressure is being driven by a significant “supply shock” in global oil markets, which saw automotive fuel prices surge by 32.8 per cent in March alone – the strongest monthly increase since the series began in 2017.

However, Ms Conisbee emphasises that the core of Australia’s inflation trouble remains tied to the housing group, which rose 6.5 per cent over the year driven by electricity, new dwellings, and skyrocketing rents.

Rental prices, which rose 3.7 per cent over the year, continue to reflect dangerously low vacancy rates across capital cities, posing one of the most significant risks to the economic outlook.

The economist highlighted a growing disconnect between monetary policy and the structural needs of the market, arguing that while higher rates can slow general demand, they do not build houses or lower the construction costs that builders are currently passing through to consumers.

In a stark warning to policymakers, she said that higher borrowing costs can actually make new housing projects less viable and discourage the very private investment needed to ease the rental shortage.

Ms Conisbee concludes that for the property market, the impact of higher rates will be mixed; while borrowing capacity will be reduced, the “severe” housing shortage and strong population growth mean that prices and rents are likely to remain supported even as market momentum slows.

The Agency Insights Partner, Cameron Kusher

The latest RBA increase means the cash rate now sits at 4.35 per cent, returning to the post-pandemic high and effectively reversing the three interest rate cuts seen last year.

The Agency Insights Partner Cameron Kusher explain that the latest data shows inflationary pressures remain elevated. With the ongoing war in the Middle East, he warned that heightened inflation is likely to persist unless demand can be eased through higher rates.

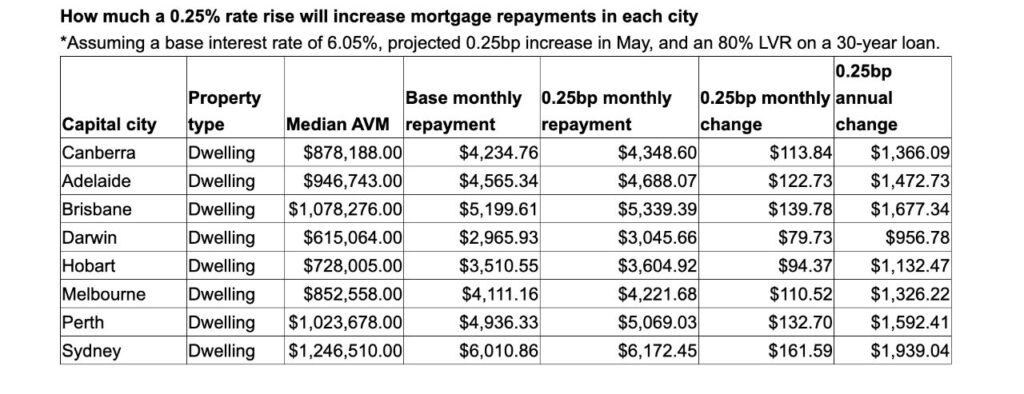

For the property market, this latest move translates to a further reduction in borrowing capacity of approximately 2.5 per cent. This brings the total reduction in borrowing capacities to around 7.5 per cent so far this year.

“For those looking to buy that have a mortgage pre-approval, this shift hastens the urgency to purchase before the pre-approval expires and likely reduces. For those with a mortgage, if you reduced your repayments last year as interest rates were cut you are now going to be facing an increase in repayments.”

For variable-rate mortgage holders who did not reduce their repayments previously, Kusher warned that the next rate increase will see their repayments rise.

The economist also emphasised that high inflation is particularly damaging because it leaves households with less money once essential goods and services are paid for.

“Higher inflation like we’re experiencing, means that goods and services cost more so once you’ve paid your mortgage and purchased all your essential goods and services there is less money leftover and that is why high inflation is so damaging and why it’s essential to curtail it.

“Unfortunately, that means a period of higher interest rates which seek to encourage households to reduce their spending, particularly non-essential spending.”

REA Group Senior Economist, Anne Flaherty

The RBA’s decision to lift the cash rate is a move described by REA Group Senior Economist Anne Flaherty as “widely anticipated given persistently elevated inflation.”

This latest adjustment marks the third rate hike of the year, a move that has now “fully reversing the cuts seen last year.”

The decision follows data showing headline CPI rose 4.6% annually over the March quarter, while trimmed mean inflation reached 3.3%, remaining stubbornly above the RBA’s 2–3% target band.

Ms Flaherty warned that the tightening cycle may not have reached its peak, noting the potential for further fiscal pain for Australian homeowners.

“With inflation expected to remain elevated, there is a strong possibility that interest rates could move even higher in 2026,” she said. “For mortgage holders on variable rates, this will add further pressure to already stretched household budgets.”

The impact is already translating to the broader property market, where the combination of reduced buyer power and higher servicing costs is cooling values.

“Higher interest rates are also reducing borrowing capacities which is already placing downwards pressure on home prices,” she said. “National home prices slipped 0.1% in April and higher interest rates will add further downwards pressure to prices.”

Domain’s Chief Residential Economist, Dr Nicola Powell

Domain’s Chief Residential Economist, Dr. Nicola Powell, noted that a rate rise was “firmly on the cards” today because the RBA could no longer afford to downplay the lack of improvement in underlying inflation.

Crucially, inflation was already gaining momentum and reaccelerating before geopolitical tensions in the Middle East escalated, raising the risk that price pressures could push back above 5% in the near term.

Dr. Powell highlighted that entrenched cost pressures and tight labour markets are being compounded by higher fuel costs.

These costs are expected to “feed directly into household expenses” and spill over into the broader economy, lifting the price of various goods and services. This deteriorating outlook has made it increasingly difficult for the RBA to look through renewed price volatility.

For the property sector, the immediate consequence of higher rates is a further squeeze on borrowing capacity and a deterioration in affordability.

Dr. Powell identified Sydney and Melbourne as the markets most sensitive to these movements due to higher debt levels and rising supply, which is currently “giving buyers more choice and reducing urgency”.

The economist observed that demand is already softening among rate-sensitive segments of the market.

“First‑home buyers, highly leveraged purchasers and debt‑dependent investors will be the first to pull back,” Dr. Powell said.

“Higher rates cap price growth by tightening serviceability and risk reigniting construction cost pressures at a time when new housing supply is desperately needed”.

LJ Hooker’s Head of Research, Mathew Tiller

Property market activity is expected to slow over winter following the Reserve Bank of Australia’s decision to lift rates but there could be a silver lining for buyers.

LJ Hooker’s Head of Research, Mathew Tiller said the RBA has acted to stay ahead of the inflation risks driven by the global conflict, which is currently at 4.6 per cent and well above its target 2-3 per cent.

The RBA’s announcement sees the cash rate return to its 2024 peak; however, it is occurring in a difficult time for many mortgage holders who are struggling with cost of living.

“The conflict is pushing up fuel and energy prices, lifting inflation again and this is broadening into transport, construction and everyday costs,” Mr Tiller said.

“Higher interest rates will see borrowing capacity fall again and in the short-term impact confidence and soften price growth. There will be more listings on the market and less competition between buyers. But the positive is that will give those looking to purchase more choice and more time to decide after a period of such tight stock levels.”

Latest Cotality figures show latest auction clearance rates in Sydney and Melbourne were 60 per cent and 61.8 per cent respectively.

Mr Tiller said the data indicates that vendors who are positioning and pricing their property to meet the market are selling.

“Buyers are still out there and while it may not be a massive number that will push up prices higher, we see them turning up at auctions and inspecting open homes,” he said.

“We expect property will be transacting throughout winter, but it will be at a different pace. Any moderation in price growth might almost negate the rate rise in some markets. This means that buyers with pre-approval may still be able to find something within their budget without having to go back to the bank.”

BresicWhitney CEO Will Gosse

Three rises this year represent a material shift in what buyers and sellers are navigating compared to three to six months ago, said BresicWhitney CEO, Will Gosse.

Affordability, as a by-product of mortgage serviceability, remains the central pressure, and today’s decision adds to that.

“What’s worth remembering is that it’s not macroeconomic conditions alone that influence the market, but the sentiment that comes with them. Even with the increase in rates, the picture becomes clearer for those looking to participate.

“That brings more incentive for buyers and sellers to find common ground and reach mutually beneficial outcomes. Decisions that may have been paused are more likely to progress.”

He expects results and activity across May and June will reflect this shift, particularly after the pronounced disruption in April.

“What we’re seeing across the major Sydney markets tells us buyer intent and demand are still present, even if the path to sale looks different.”

Oliver Hume Property Group Chief Economist, Matt Bell

Oliver Hume Property Group Chief Economist, Matt Bell said that before the decision, markets had priced in ~70% chance of the hike, with all big four banks forecasting the increase.

“We’re now exactly where we were before the three rate cutting cycle began in February 2025, with a wide range of forecasts about the rest of 2026. Westpac has two more rate hikes forecast for 2026, while the other three big banks think this will be the last increase.”

What does this mean for property markets?

Early signs are not as dire as initially feared. Mr Bell said we’re still seeing strong price rising in those already booming housing markets of Perth, Brisbane and Adelaide, and even in Sydney and Melbourne, where prices are easing, they’re still rising in the most affordable suburbs.

In the land space, March quarter volumes eased in those overheated markets, but this was because of supply constraints, with demand holding up well as indicated by strong price rises. In Melbourne, volumes and prices held at late 2025 levels.

Other indicators have also held up.

“Auction clearance rates and consumer sentiment are up off the lows seen at the start of the Middle East crisis. New home sales rose in March, and unemployment has held steady at historically low levels,” he said.

“Clearly the outlook for property in 2026 is worse than it was before the crisis began, but with fuel prices well below their March peaks and supply largely sorted for Australia, it seems it will be a stabilisation in rate expectations that will settle the market before returning to normal activity in late 2026 or 2027.”