The Australian housing market has entered a more complex phase, hit by a simultaneous cyclical and structural shock that is splitting the nation’s property landscape into fragments.

Following three unexpected interest rate hikes in the first half of 2026 that pushed the cash rate to 4.35%, a sweeping federal budget overhaul has accelerated a market-wide divergence.

The removal of negative gearing from established properties alongside adjustments to the Capital Gains Tax (CGT) discount has introduced a structural shift that is actively reshaping household budgets, consumer confidence, and borrowing capacities nationwide.

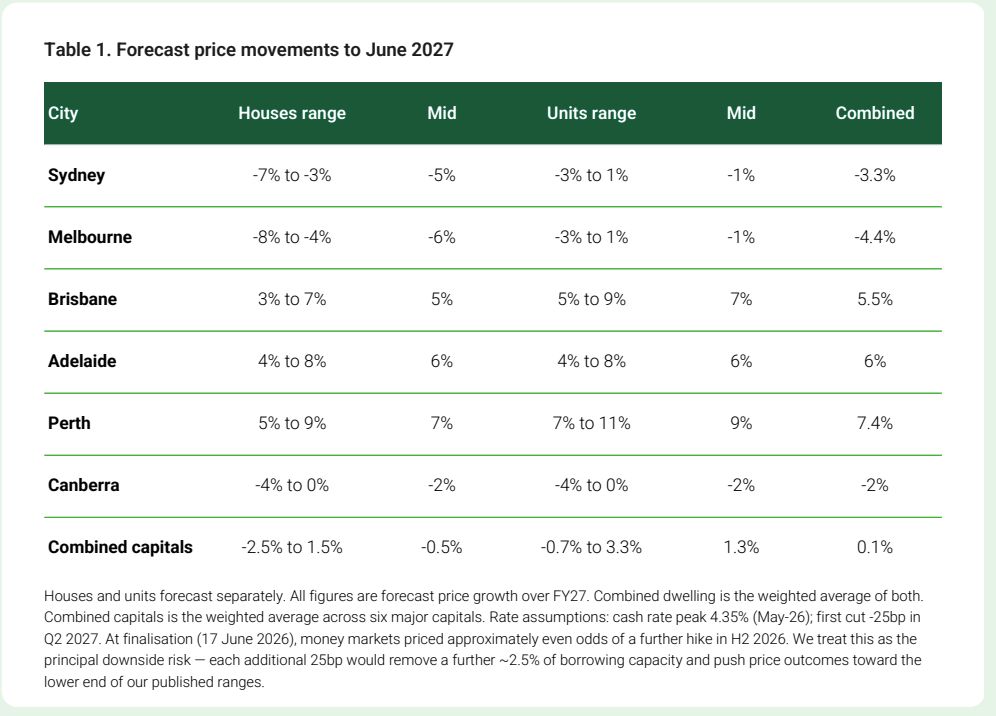

The fallout is far from uniform. Rather than a blanket national slowdown, a sharp divide has emerged between capital cities with differing affordability profiles, investor exposures, and supply dynamics. Sydney, Melbourne, and Canberra houses are on a definitive downward trajectory.

Conversely, Brisbane, Adelaide, and Perth continue to see values grow, though at a fraction of the extraordinary run rates recorded during their recent booms.

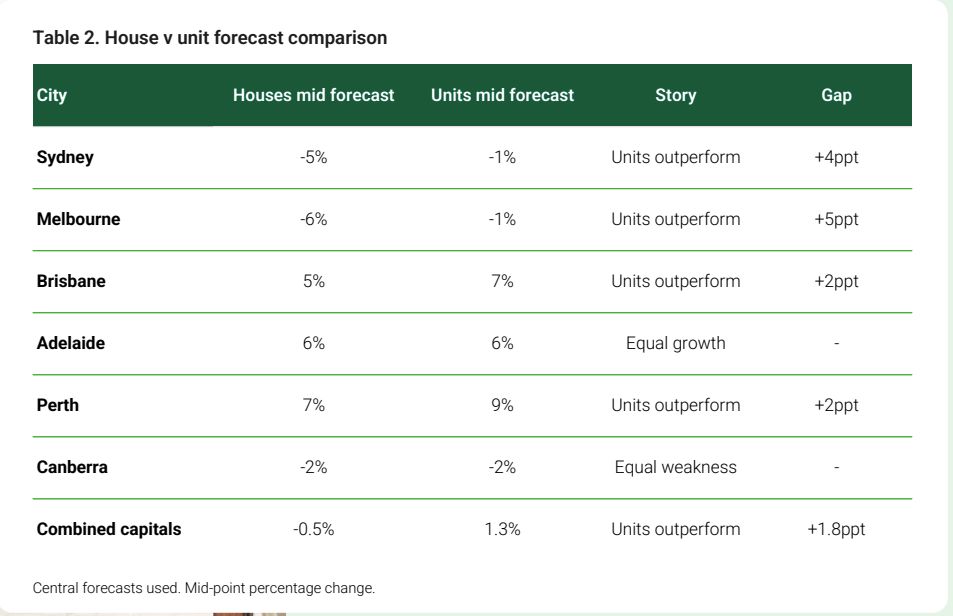

Across nearly all capital cities, unit prices are holding firmer than detached houses as affordability pivots from a casual consideration to a binding economic constraint.

With inflation remaining exceptionally stubborn – headline CPI sits at 4.2% and the RBA’s preferred trimmed mean indicator is stuck at 3.4% – borrowers are currently being assessed at mortgage rates near 10% under APRA’s mandatory serviceability buffers.

Data: Domain

This borrowing power shock has stripped roughly 7% to 8% from a typical buyer’s purchasing capacity, forcing a stark behavioural pivot.

Buyers are trading location for value, shifting demand away from premium freestanding homes toward more accessible apartments.

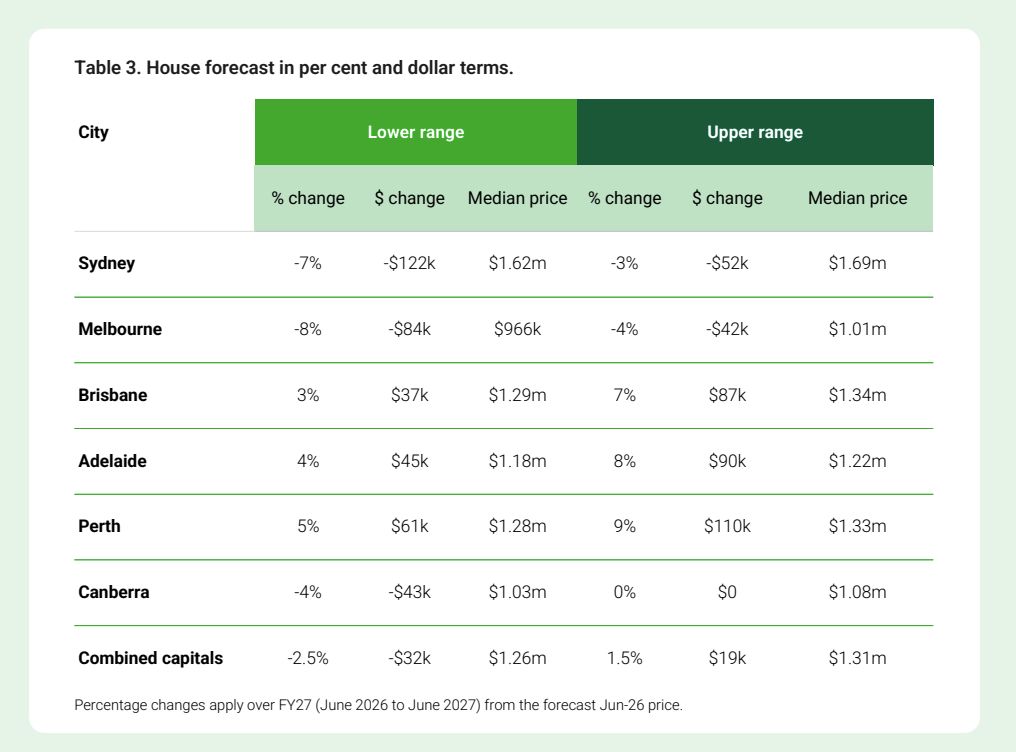

Sydney is leading the multi-tier market correction; its house prices are projected to fall between 3% and 7% over FY27, equating to a drop of $52,000 to $122,000.

Melbourne faces a steeper mid-point contraction of 6%, with house prices forecast to drop between $42,000 and $84,000, a move that could potentially push the city’s median house price below the $1 million mark for the first time since 2021.

Canberra is similarly softening, with house prices projected to slide up to 4%, or a drop of up to $43,000.

Data: Domain

Yet, where freestanding houses are stumbling, units are dramatically outperforming.

Due to a record 111% house-to-unit premium and expanded first-home buyer schemes, apartment demand is surging.

Sydney and Melbourne unit declines are expected to remain tightly contained to a minor 1% mid-point drop. In a stunning geographic shakeup, Brisbane’s unit market is forecast to jump 5% to 9%, overtaking Sydney to officially become Australia’s most expensive unit market.

This dramatic shift highlights the core theme of Domain’s latest report: lower borrowing capacity doesn’t erase property demand; it simply redirects it.

Data: Domain

“The housing market is no longer moving in lockstep. Higher interest rates are weighing heavily on Sydney and Melbourne, while more affordable segments and mid-tier cities are continuing to hold up,” said Domain Chief Residential Economist, Dr. Nicola Powell.

“The outlook remains closely tied to the path of interest rates. We expect the RBA to hold rates through the remainder of 2026, with the first rate cut likely in mid-2027, although the risk of a further hike remains if inflation proves more persistent.

“That will be a key turning point for the housing market. Until then, affordability constraints will continue to shape both price growth and buyer behaviour.”

Meanwhile, severe supply deficits, tight rental pipelines, and interstate migration are shielding the smaller capital cities from the broader downturn.

House prices in Brisbane (up 3% to 7%), Adelaide (up 4% to 8%), and Perth (up 5% to 9%) are all tipped to hit new record highs over the coming financial year.

However, analysts warn these growth corridors carry hidden vulnerabilities. Investor home lending in Western Australia has skyrocketed to 39.1% – a massive 14 percentage points above its long-run decade average.

Queensland and South Australia are similarly overexposed, sitting 9.7 and 12 percentage points above their historical norms.

If investor sentiment sours further in response to the federal budget’s July 2027 negative gearing restrictions, these growth markets could face a sudden, sharp withdrawal of capital.

The remainder of 2026 is forecast to stay weak, characterised by falling transaction volumes as buyers and sellers pause to recalibrate.

While an improving rental yield profile may attract yield-focused buyers back to units by early 2027, any meaningful market recovery remains entirely contingent on the RBA delivering its first rate cut by the June quarter of next year.

If sticky inflation forces another interest rate hike instead, borrowing capacity will contract by an additional 2.5%, threatening to drag Australia’s housing market well below its current forecast ranges.