New analysis from Cotality reveals that the expanded first home buyer deposit guarantee scheme appears to be intensifying competition at the lower end of the housing market, with eligible properties outpacing growth in higher-priced homes by a significant margin.

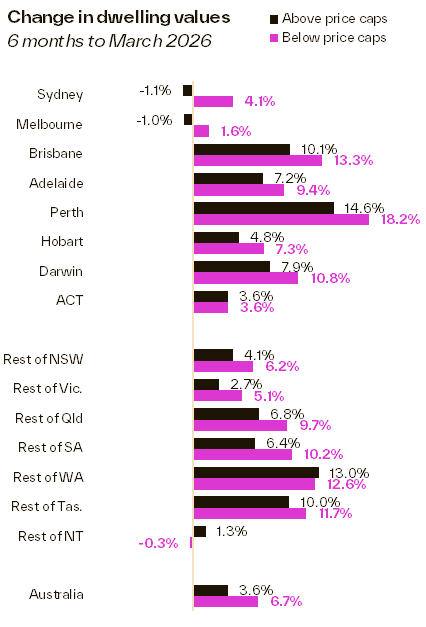

Since the scheme was expanded on 1 October last year, properties with values below the price caps have increased by 6.7 per cent, compared with just 3.6 per cent growth for homes above the thresholds.

“The divergence started opening around the time of the announcement in late August,” the Cotality Research Director, Tim Lawless, said, suggesting buyers began moving early in anticipation of increased competition.

The pattern is consistent across almost every market in Australia – 81 of 88 sub-markets (92 per cent) have recorded stronger growth for properties under the price caps.

Sydney recorded the starkest divide. Homes under the $1.5 million cap rose 4.1 per cent over six months, while those above fell 1.1 per cent – a 5.2 percentage point gap.

Mr Lawless said there were several factors driving the imbalance.

“Anticipation of increased competition and price pressure after the scheme’s launch has likely brought forward demand from those who didn’t necessarily need to rely on the deposit guarantee,” he said.

Serviceability constraints are also pushing buyers toward cheaper properties, with elevated interest rates limiting borrowing capacity.

And investors are adding to the squeeze – they comprised 40 per cent of mortgage demand in the December quarter, well above the decade average of around one-third.

The scheme’s effectiveness may already be waning.

At the end of September, 48.6 per cent of suburbs nationally had a median house value below the price caps. By March, that had dropped to 39.5 per cent.

Darwin, where price caps weren’t adjusted in October, now has just 10.3 per cent of suburbs with a median house value under the $600,000 threshold – down from 32.4 per cent in September.

Perth is close behind at 11.6 per cent, down from a third of suburbs six months earlier.

“Despite its sheer unaffordability, Sydney has the highest portion of suburbs where the median house value falls below the price caps,” Mr Lawless said.

At 46.8 per cent, this is partly explained by the city’s higher $1.5 million cap – more than $500,000 above any other capital – and partly by relatively flat growth of just 0.4 per cent over six months.

Beyond finding an eligible property, first home buyers face a growing finance challenge.

The average first home buyer loan increased 7.7 per cent in the December quarter to $606,400. With interest rates rising half a per cent since then, borrowing capacity for a household earning $100,000 has fallen by approximately $34,300.

With the three-percentage-point serviceability buffer applied to the March average variable rate of 6.01 per cent, buyers must demonstrate they can service a mortgage at around 9 per cent or higher.

“Overall, it is likely first home buyer deposit guarantee will gradually lose its stimulatory power, with more homes exceeding the price thresholds and a growing portion of prospective buyers running into a finance hurdle that is set to rise further,” Mr Lawless said.