The country is now home to at least 162 operational data centres, with a further 90 projects in development, placing Australia among the fastest-growing data centre markets globally outside the United States.

At the same time, new Australian Bureau of Statistics figures show residential building approvals fell 5.7 per cent in May, with the housing construction pipeline continuing to fall behind national targets.

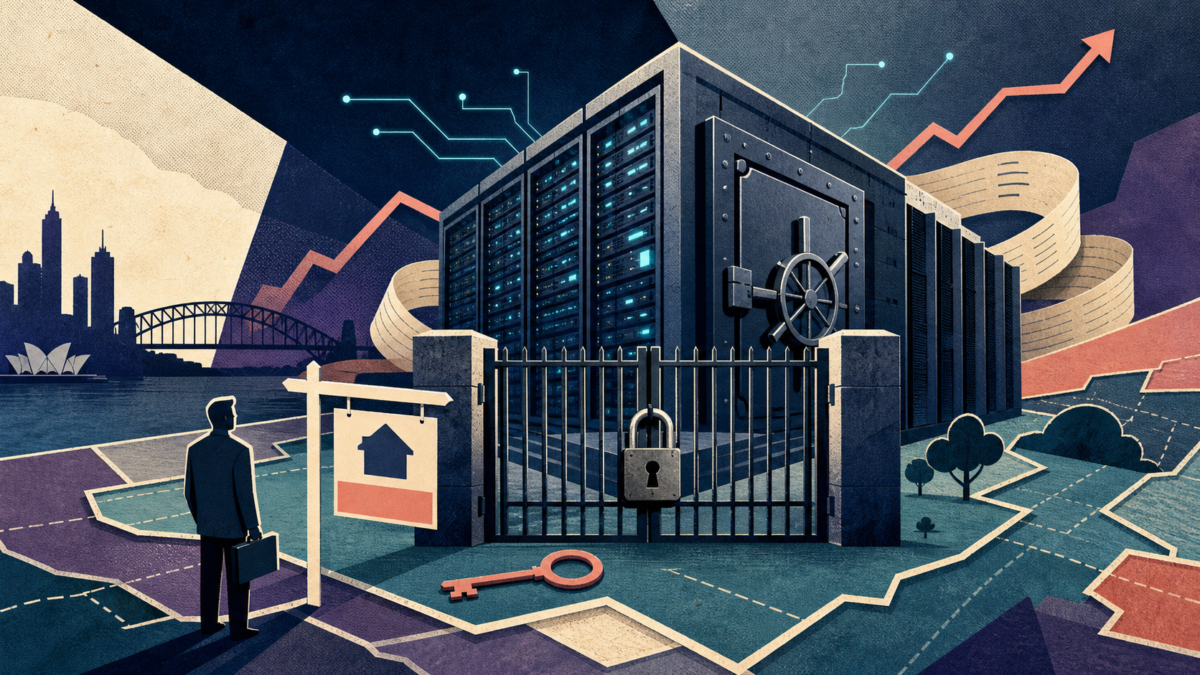

The diverging trends highlight a growing structural tension between Australia’s housing shortfall and the rapid expansion of AI-driven digital infrastructure.

The data centre boom has effectively arrived on Australian shores, transforming from a subset of industrial property into a standalone institutional asset class almost overnight.

To the untrained eye, Australia’s vast landscape looks like the ultimate frontier for a massive land grab as tech giants like Google, Microsoft, and Amazon look to pour billions into cloud and artificial intelligence infrastructure.

But behind the high-security gates, the reality on the ground is a fiercely competitive, highly restricted game of power, politics, and property.

“They are a very hard asset to try to get your head around, to be completely honest,” says Vanessa Rader, Head of Research at RWC.

“It has been industrial asset for many, many, many years, but in the last, let’s call it eighteen months, it’s kind of formed its own asset class in its own right.”

For the everyday commercial real estate sector, getting a foot in the door means looking past the hype and understanding the brutal physical constraints governing the asset class.

Data centres are fundamentally bound by a strict trio of requirements: connectivity, power, and water and Vanessa jokes that you can’t simply buy a cheap plot in the outback and start digging.

“You can’t just stick one in the middle of nowhere,” she says. “Connectivity and energy are two very big things. If you just stuck a data centre within our existing energy grid, the whole city would shut down.”

It is why development remains intensely concentrated in hyper-specific hotspots like Sydney’s Macquarie Park, Melbourne’s industrial corridors, or coastal zones in Western Australia and the Sunshine Coast that tap directly into subsea cables to Asia and Japan.

“The technology changes so rapidly and so quickly, and a lot of these assets will continue to evolve and need to be kept up to date.”

Because these behemoth assets are so capital-intensive, they are largely the playground of major funds and trusts.

“The asset size is very big, so it’s prohibitive for a lot of people to invest in the asset class, just because of the sheer cost involved,” Vanessa explains.

The upside for these institutional investors is unmatched stability: while traditional office or retail spaces face constant tenant turnover, a data centre occupier typically signs on for a rock-solid 10 to 20 years.

“Your tenant is pretty much going stay there for the next ten, fifteen, twenty years,” Vanessa says and this bulletproof security has compressed yields as low as 4%, making them the tightest asset class in the country.

“They’re probably the lowest yielding asset class at the moment because they are just these very big behemoth type assets that are held onto for a very long time.”

Furthermore, strict data sovereignty laws mean international buyers face heavy restrictions.

“They can only really be invested in Australia by Australian funds because there’s a lot of issues around data sovereignty.

“Overseas buyers can’t necessarily go and buy a data center when it’s Australian data that’s involved with them.”

The coming regulatory storm

As hundreds of millions of dollars in computing investment prop up the broader economy, the federal government is moving fast to ensure the grid can actually handle the strain.

Data centre electricity consumption is projected by the Australian Energy Market Operator (AEMO) to triple by 2030, a massive surge equivalent to the power needs of every home in Victoria.

To protect everyday consumers, the government is introducing a strict “triple-lock” set of obligations for new developments, designed to turn these energy-guzzling hubs into grid assets rather than grid burdens.

New & Clean Supply

Tech giants must bring or fund their own renewable energy generation; they cannot simply drain the public grid.

Network Cost Coverage

Operators must pay their full share of grid connection costs so the financial burden never trickles down to households.

Demand Flexibility

Facilities must act as a grid asset. During peak times (like extreme weather events), they will be forced to wind down power use so the grid doesn’t collapse.

This legislative pivot completely shifts the development landscape.

Future data centres will not just be warehouses full of servers; they will double as private energy hubs and this ties directly into the rising corporate focus on sustainability.

“Particularly with institutional investment, ESG (Environmental, Social, and Governance) is super important,” Vanessa says. “A lot of these have been purchased by the funds and institutions, which have very strong policies around ESG … so they can’t really put these assets in their portfolios unless they are true to whatever their mandates are.”

During peak summer or winter days when the public grid strains, these facilities will power down their primary usage, allowing the privately funded solar and wind farms attached to them to feed clean electricity directly back to everyday Australian homes and businesses.

Hunting the golden ticket

With tech giants dealing directly with major institutional developers under strict confidentiality agreements, where does the grassroots real estate industry fit in?

“A lot of these transactions happen probably excluding a lot of agents to be fair, because they are just high profile, high security, high confidentiality type transactions.”

However, Vanessa says the frontline opportunity for savvy commercial agents lies squarely in site identification.

Finding industrial-zoned land that miraculously checks the boxes for high-voltage power capability, water access, and fiber-optic connectivity is the ultimate golden ticket in the current market.

“Site identification would be one thing… for an agent, that’s probably the best thing they can do.”

At the same time, the industry is preparing for a creative shift toward smaller, localised “edge” data centres.

“Are we going be in a position where we need smaller, more local data centres? That’s a legitimate question.”

As regional and inner-ring metropolitan demand grows for faster processing speeds, the sector may see unique adaptive reuse opportunities.

“That could be kind of alternative use for other assets, maybe like office buildings or something, I’m just being a bit creative here of what I’m thinking.”