The narrative surrounding Australia’s property market has taken a distinctly ominous turn lately. High interest rates are digging in, global economic ripples are creating widespread caution, and recent federal budget changes targeting property investors have left many wondering if the great property boom is finally hitting a brick wall.

But if you look past the sweeping national headlines, a much more fascinating and entirely uneven story is unfolding.

The property market isn’t just slowing down; it’s fracturing into completely different dynamics depending entirely on who owns the streetscape.

While high density investor markets are visibly cooling, a quiet revolution is happening on the fringes of our capital cities.

In middle and outer ring suburbs driven not by landlords, but by everyday families buying a place to live, prices are accelerating toward the million dollar milestone with remarkable momentum.

The fallacy of the uniform downturn

When the federal government dialed up the pressure on property investors in the budget, the knee jerk assumption was that the entire housing market would retreat in unison.

“The main misconception is around investors,” said Ray White Economist Atom Go Tian.

“The biggest loser of these budget changes are your investors, and the assumption is that because investors are going to retreat from the market, the entire market will begin to slow down.”

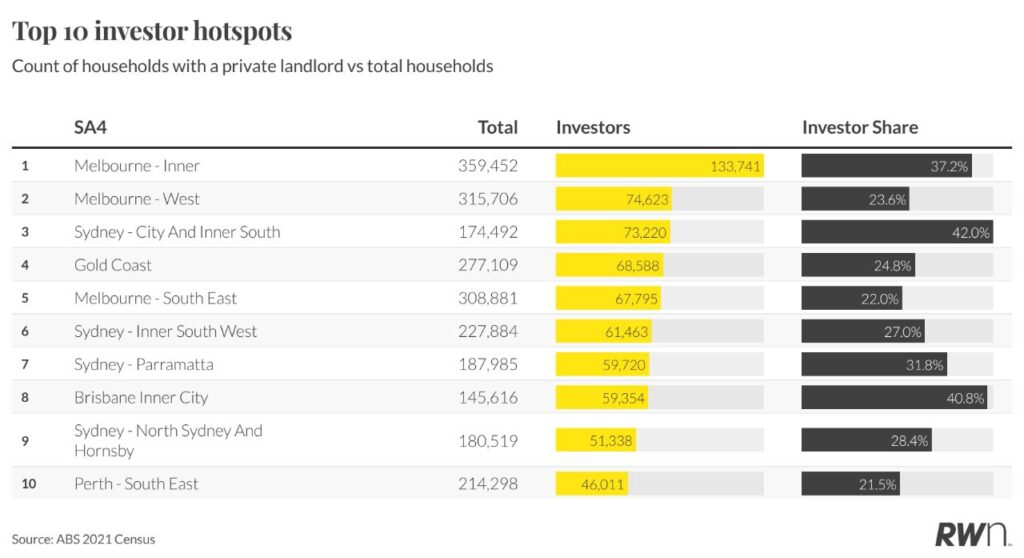

That view misses a fundamental structural reality: investors are not evenly distributed. Landlord capital is heavily concentrated in specific investor bubbles, predominantly premium, inner city, unit dominated markets like Melbourne Inner, Sydney City, or Brisbane Inner City, where investors hold up to 42 per cent of the stock.

Because these areas are so heavily exposed to investor sentiment, they are bearing the brunt of the policy shift; nearly a third of suburbs with high investor concentrations have already slipped into negative growth.

“What we’re noticing is that there are actually these bubbles for investors, and they normally concentrate in your inner city markets,” Mr Tian said.

“So the expectation is that these areas will be the hardest hit, but that doesn’t mean all of Australia will be hit evenly. Where investors are thin, the pullback has less to work with.”

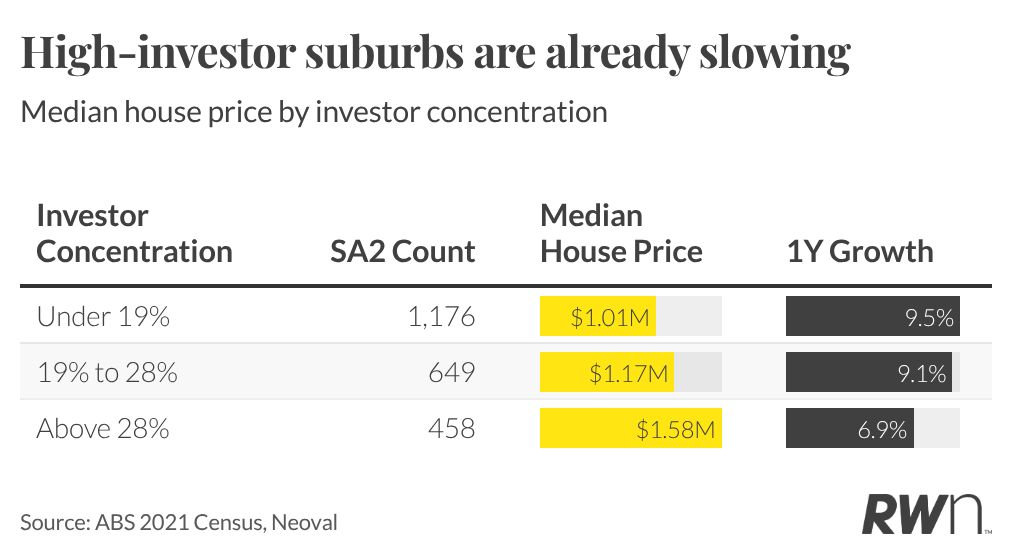

Step outside these inner ring bubbles into the suburbs where investor exposure drops below 19 per cent, and the market dynamics flip.

These are the owner occupier strongholds, and they are outperforming landlord heavy markets across the country.

Suburbs with the highest investor concentrations are already recording a weaker annual growth rate of 6.9 per cent, compared to a robust 9.5 per cent for the lowest investor band.

Mr Tian said that these investor heavy pockets are facing a double whammy: “Not only are they struggling from premium pricing, but then they’re also going to be struggling from a retreat in buyer activity.”

Chasing the sweet spot

Right now, the absolute sweet spot for local agencies sits firmly between $750,000 and $1 million. It’s the band where buyer demand remains fiercely resilient.

“Your affordable areas, typically from $750,000 to $1 million, that’s your sweet spot of affordable but still attractive,” Mr Tian said.

“And so these areas are seeing your biggest growth. Normally, in major cities, these are your outer suburbs.”

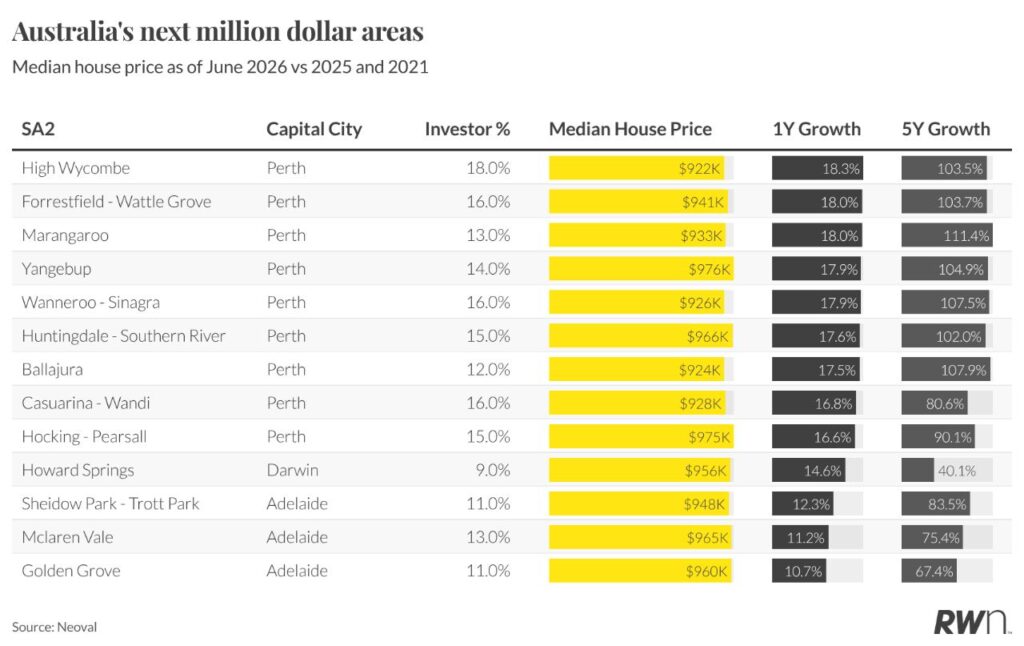

Take a suburb like Marangaroo in Perth’s northern suburbs, where a typical home there costs $933,000. Even if its current growth rate halves over the next year, it is mathematically locked in to cross the million dollar threshold within the next 12 months.

Marangaroo is not an anomaly; it’s part of a broader migration of capital. Because the inner rings of cities like Perth and Adelaide have already priced out the average buyer, demand is radiating outward into previously affordable, community minded suburbs.

“You’ll notice that with these suburbs in Perth, they’re also towards the outer suburbs,” he explains.

“And so we are seeing that there is an expansion in this affordability frontier. It’s moving outward, and as prices are growing in the inner suburbs of Perth, these areas, which typically are owner occupier suburbs, are seeing that massive growth. And then the same thing you’ll notice in Adelaide as well.”

In Adelaide, places like Golden Grove in the northern growth belt, alongside Sheidow Park Trott Park and McLaren Vale in the south, are seeing double digit annual growth despite the broader economic chill.

They carry microscopic investor shares, between 11 and 13 per cent, meaning their growth is entirely organic, powered by locals buying homes to live in.

Even Darwin has thrown a contender into the ring. Howard Springs, sporting a bare 9 per cent investor exposure, has spiked 14.6 per cent over the past year to sit at a median of $956,000. It stands as the lone northern defender marching steadily toward the million dollar club.

Notably absent from this shifting frontier are the big three eastern capitals. Sydney, Melbourne, and Brisbane have effectively bypassed this phase of the cycle.

Their traditional owner occupier belts passed the million dollar mark years ago, while their remaining affordable pockets carry high investor density, leaving them exposed to the current slowdown.

“On the national level, there’s this trend of premium suburbs having the slower growth,” Mr Tian said.

“When you look at major cities, there’s the same pattern. Sydney and Melbourne are premium relative to other cities and over the last few years, they have been much slower.

“On top of that, most of the suburbs in Sydney, in particular, are already above a million dollars, and so that’s why they’re not in the list.”

For principal directors and listing agents trying to time this fragmented market, looking at median settled prices is like looking in the rearview mirror. To see where the market is actually heading, Mr Tian looks at leading operational metrics before the final sale ever takes place.

“There are really three key metrics that we like to look at,” he said.

“First is your open home inspection. The number of people showing up to your open homes, because this is your leading indicator of sentiment. Over the last six months, we have been seeing lower numbers of attendees, and so this is really capturing that sentiment of caution. The second is your time on market, and your third is your listing volume. Those give you a head start on where the market is going to follow.”

The ultimate glass ceiling

While these owner occupier sanctuaries are beautifully insulated from the investor exodus, they are not entirely bulletproof.

The real threat to their ongoing boom isn’t a shift in government policy; it’s the harsh reality of the household budget and Mr Tian points out that a structural balancing act is currently taking place, observing that “there is now appearing to be a very distinct ceiling, but then a distinct floor as well to the market.”

At a median value hovering between $920,000 and $975,000, these entering million dollar suburbs are rapidly approaching the absolute financial ceiling of what a working family can comfortably finance in a high interest rate environment.

When asked which macroeconomic force will ultimately shape the next few years the most, he points directly away from short term noise and toward structural shifts.

“It’ll definitely have to be the changes to investor policy,” he said.

“Your interest rates and your global uncertainty, those tend to affect your short term sentiment much more, because they fluctuate pretty rapidly, whereas your budget policy change, that’s something quite permanent and long term. So that will be affecting how the market behaves over years and not just months.”