This week I was struck by a suggestion that Melbourne’s relative affordability is largely the result of taxes and policy settings that have made Victoria less attractive to investors. It’s a simplistic explanation that seems to be gaining traction – effectively attributing affordability to the absence of investors – but one that doesn’t hold up to the data.

Melbourne’s affordability hasn’t been created by taxes; it has been built. Over an extended period, Victoria has delivered more housing than any other state, and that sustained development pipeline has kept price growth less elevated than elsewhere.

What higher taxes on investors have done is not create affordability, but change how it is distributed – delivering more of the benefit to home buyers, while renters face tighter supply and much stronger rental growth.

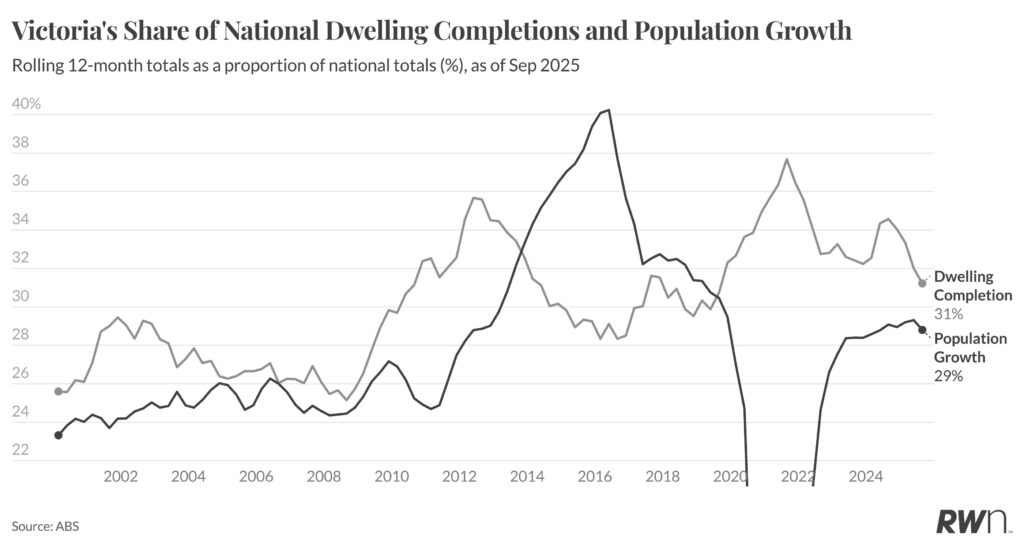

The scale of how much supply has been created has been significant. Since 1984, Victoria has completed more homes than any other state in Australia, and in more recent years that lead has widened. Over the past decade, just over 30 per cent of all new homes built nationally have been delivered in Victoria, despite the state accounting for only around 27 per cent of population growth over the same period.

This is not a short-term surge, but a sustained expansion in construction capacity and planning settings that have allowed new housing to be delivered at scale.

While other states have struggled to keep up with demand, Victoria has consistently added supply – and that has made a material difference to how its housing market has performed.

The impact of that supply is clear in the data. Melbourne hasn’t avoided rising housing costs – but it has seen far more subdued growth than the rest of the country. Price growth has been the lowest of any major capital city over the past five years, and rental growth has also been lower than in most other large markets, particularly compared to the sharp increases seen in high-growth states such as Queensland, South Australia and Western Australia.

This is what strong supply does. It calms growth in both prices and rents. In a country struggling with affordability, the lesson is straightforward: if you want to keep housing costs under control, you have to build more of it.

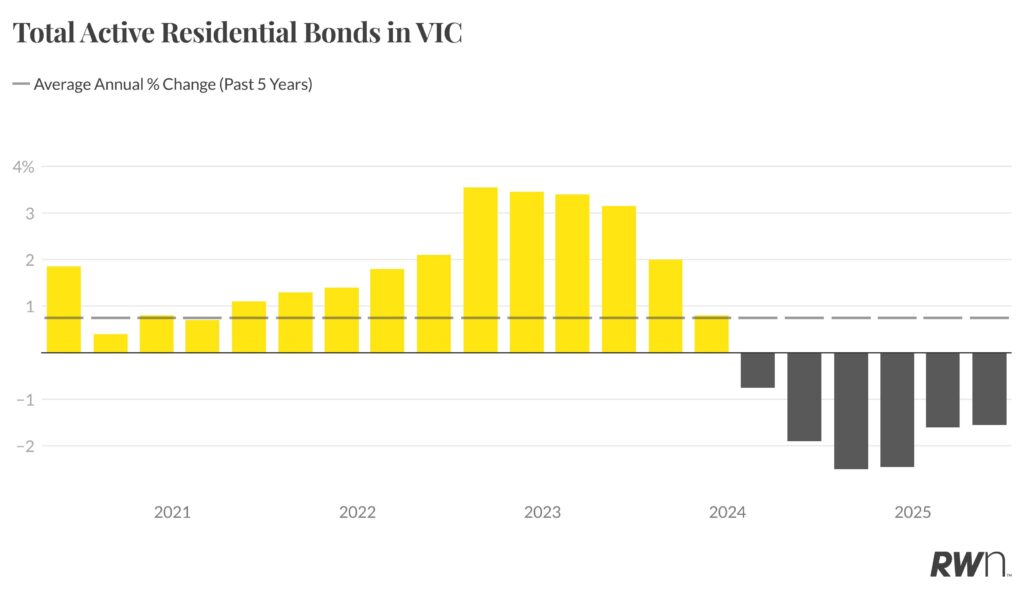

So what have higher taxes on investors actually done? They have reduced the number of rental properties. After peaking at around 676,000 bonds in mid-2023, the number fell to around 655,000 by mid-2024 – a loss of more than 20,000 rental properties in the space of a year. That is a material contraction in supply. The result has not been greater affordability overall, but a redistribution of it. Home buyers have benefited from weaker price growth, while renters have faced tighter conditions and stronger rent increases. The pressure hasn’t disappeared – it has just moved.

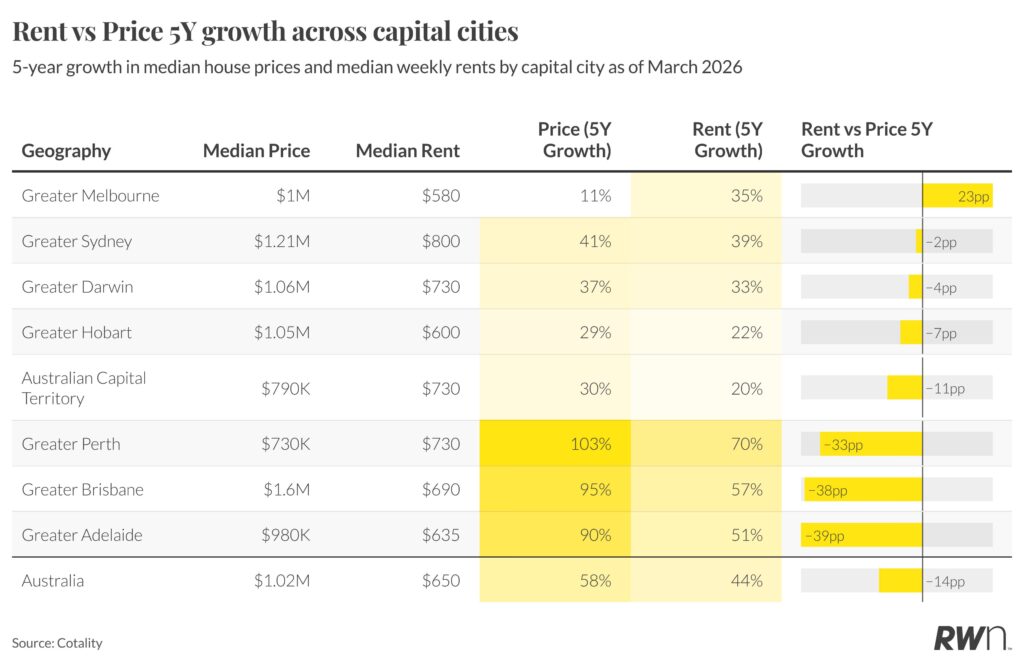

The scale of that shift is clear when comparing price and rental growth across capital cities. In every major market, price growth has significantly outpaced rents over the past five years, reflecting the impact of tight supply being capitalised into asset values.

Melbourne is the exception. Over the past five years, price growth has been just 11 per cent, while rents have risen by 35 per cent, moving in the opposite direction. This is a fundamentally different outcome. In most cities, housing pressure has shown up in prices. In Melbourne, it has shown up in rents.

Why does this matter? Because housing policy doesn’t just determine affordability – it determines who bears the cost of it. Victoria has shown that building more homes can materially improve affordability by keeping both price and rental growth more contained than elsewhere.

But policy settings that discourage investors don’t remove housing pressure – they shift it. In this case, the benefits of stronger supply have flowed more to home buyers, while renters have faced tighter conditions and higher rents.

And renters don’t simply disappear. They are typically younger, lower-income, and more exposed to rising costs.

The consequences are long-term. Those who reach retirement while still renting are far more likely to experience financial stress and poverty, and higher rents only make that outcome worse. Shifting affordability from prices to rents doesn’t solve the problem – it moves it onto those least able to absorb it.

The broader implication is clear. If similar policy settings were applied at scale in areas with strong population growth such as Queensland, Western Australia and South Australia, the outcome would likely be very different to Victoria. These states have experienced much stronger price growth precisely because supply has been more constrained.

Reducing investor participation in these markets would not solve affordability – it would tighten rental supply further and place even more pressure on rents. In fast-growing markets, where population growth is strong and supply is already struggling to keep up, discouraging investors risks amplifying the rental crisis rather than easing it. The pressure doesn’t disappear – it intensifies where supply is weakest.

Despite being more affordable than many other parts of the country, Victoria’s broader economic position is more challenging – and this is also weighing on house price growth.

Business confidence is the lowest in the country, while government debt continues to rise, increasing pressure on state finances.

Population growth remains strong, but is now almost entirely driven by overseas migration, with more than 80,000 residents lost to other states over the past five years, many to stronger markets such as Brisbane and Perth.

For residents, houses may be cheaper but conditions are tougher. Unemployment is now the highest in the country and one in eight young people are now unemployed, with only the Northern Territory seeing more young people without jobs.

Not surprisingly, this is flowing through to consumer stress which is also amongst the highest in the country.

The economy is becoming increasingly uneven, with a growing divide between those supported by public sector employment and those exposed to weaker private sector conditions.

There is also a risk to this model that has maintained affordability. A strong development pipeline depends on a confident and profitable private sector.

With business confidence low, costs rising and taxes increasing, the economics of building are becoming more challenging. Policies that discourage investors also affect the feasibility of new projects, particularly in higher-density development.

Over time, this risks slowing the pace of construction. If supply begins to weaken, the affordability gains Victoria has achieved will become harder to sustain.

There is, however, a clear positive in Victoria’s experience. It shows that housing affordability is not out of reach – but it also makes clear where it comes from.

It isn’t the result of higher taxes or discouraging investors. It is the result of building more homes, consistently and at scale, over a long period of time. That supply has made a real difference, keeping both price and rental growth more contained than elsewhere. In a country defined by housing shortages, that is a meaningful achievement.

The lesson is simple: if you want better housing outcomes, you have to build.