The Australian housing market is showing “mixed signals” as total property listings remained virtually unchanged in April, according to the latest data from SQM Research.

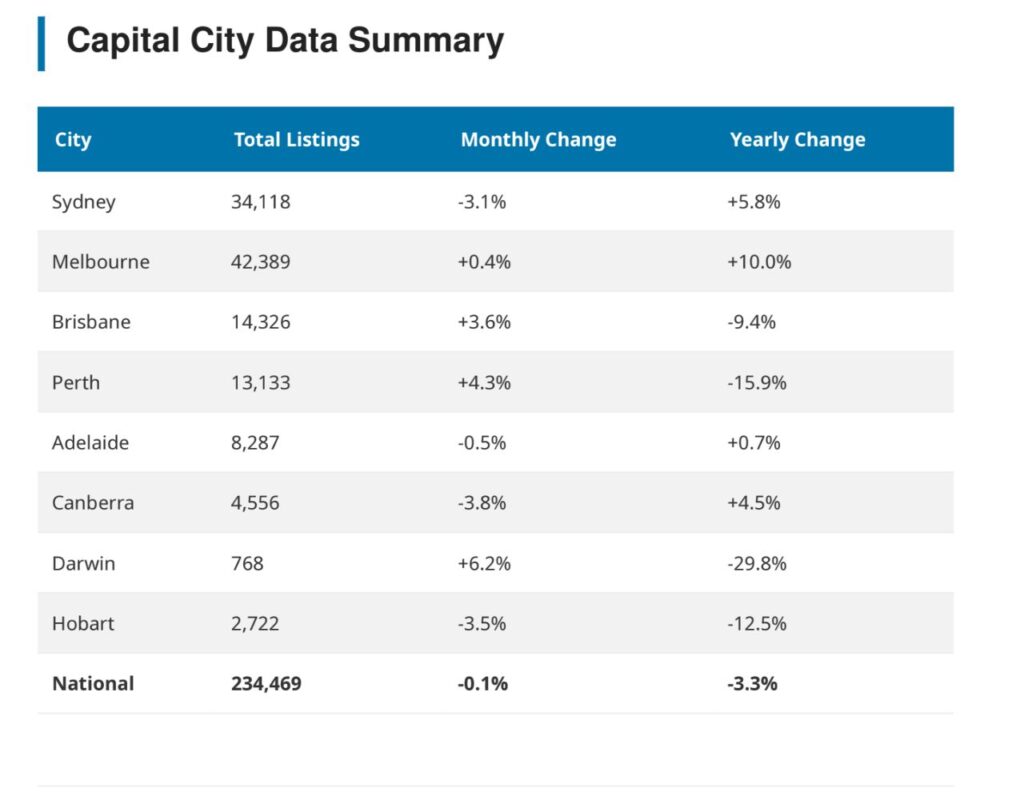

National residential stock stood at 234,469 dwellings, a marginal month-on-month dip of 0.1%. While total supply appears to be stabilising, the underlying data reveals a market in transition, characterized by a sharp drop in new listings and a steady accumulation of older stock.

The seasonal shift: new vs. old stock

The flow of fresh properties entering the market slowed significantly in April, with new listings (under 30 days) declining 6.8% nationally to 73,588 dwellings. Industry experts attribute this “pullback” to the impact of seasonal public holidays and a growing sense of “uncertainty by would-be vendors”.

In contrast, old listings (properties on the market for more than 180 days) rose by 3.6% to 66,819, suggesting that some stock is beginning to linger.

Managing Director of SQM Research, Louis Christopher said April’s figures highlight an uncertain market and one that was impacted by the seasonal public holidays.

“While total listings were broadly unchanged over the month, the composition of the data is quite mixed. We are seeing some pullback in new listings alongside a rise in older stock, which suggests vendor uncertainty and cautious buyers”.

Perth: a market to watch

While much of the country saw supply constraints ease, Perth continues to stand out. Total listings in the Western Australian capital rose 4.3% in April, extending a rebound seen in March, yet remain 15.9% lower year-on-year.

“Perth a key market to watch,” Mr Christopher said.

“There might be signs of a slowing in activity. Listings have now risen for two consecutive months, which is notable given how tight conditions have been. However, supply is still well below last year’s levels”.

Despite broader economic pressures, distressed listings remain relatively low at 3,659 properties nationally. While this reflects a 4.2% monthly increase, it is a substantial 23.7% decrease compared to April 2025.

Asking prices also showed resilience, remaining 11.5% higher year-on-year nationally. While combined dwelling prices slipped a minor 0.2% in April, Christopher noted that the market “remains supported, even as short-term conditions become more variable”.